The United States Securities and Exchange Commission has likely approved asset manager VanEck’s Bitcoin Strategy exchange-traded fund, with trading expected to begin on Oct. 25.

In an Oct. 20 filing with the Securities and Exchange Commission, or SEC, Vaneck said the public offering of its Bitcoin (BTC) Strategy ETF, which offers exposure to the crypto asset through future contracts, would begin “as soon as practicable” after the effective date of the filing, Oct. 23. This suggests the company could list its shares on an exchange as early as Oct. 25.

Unlike exchange-traded funds offering direct exposure to BTC or Ether (ETH) — which the SEC has not approved — VanEck’s ETF would provide exposure through cash-settled BTC future contracts traded on exchanges registered with the Commodity Futures Trading Commission, pooled investment vehicles, and other exchange-traded products. Having first applied for the BTC futures-linked ETF in August, VanEck could follow ProShares, which on Monday launched its Bitcoin Strategy ETF on the New York Stock Exchange.

Related: Crypto market cap breaks $2.5T — Is this the season for ETFs?

The potential VanEck ETF listing comes as BTC and ETH prices reached new all-time highs. According to data from Cointelegraph Markets Pro, the prices of BTC and ETH are $65,955 and $4,003, respectively.

Bitcoin and other cryptocurrencies, such as Ethereum, are becoming more popular as an investment alternative. In early 2021, the price of bitcoin skyrocketed to all-time highs. Bitcoin is currently worth $33,225.90.

In 2020, Bitcoin and other cryptocurrencies outpaced the majority of traditional investments.

Bitcoin and other cryptocurrency investments are well-known for yielding huge profits at high risk. Almost every investor understands the volatility of cryptocurrency, whether they invest with personal assets or retirement funds. If you are going to dabble in crypto investing, you must be informed of your acceptable loss.

Should you include bitcoin in your 401(k)?

Begman of IRA Financial stated – “Just like stocks, Bitcoin can be purchased in an IRA or 401(k). However, from a practical standpoint, an employer-adopted 401(k) plan with employees will likely not allow for any alternative investment options because of ERISAfiduciary rules.”

Even so, people who want to add cryptocurrency to their 401(k) should think about a few things first.

According to Leanna Haakons, the Founder of Black Hawk Financial, the biggest benefit would be that people interested in crypto could invest pre-tax money, something they cannot do through a brokerage account at this time. This is something long-term investors will benefit from. However, some self-directed IRAs do offer bitcoin as an investment option.

In addition, Haakons added that because retirement plan providers cap crypto contributions at 5% of an account’s total value, it is a smart way to get engaged in crypto investing without risking too much of your money, as you might if you invested on your own and went all in.

Lyle D Solomon

Haakons added that the at-home investor who is not going to be monitoring the market every day is a better option. They should be given the exposure and the chance to make some of those big potential gains but restrict them to follow the guidelines.

Cryptocurrencies, like bitcoin, are extraordinarily volatile assets. A 401(k) or individual retirement plan should be made up of stable, low-cost investments you feel will grow in value over time. That means index funds are one of the best choices for most average investors.

With a few exceptions, you will not be able to take money out of your 401(k) until you are above the age of 59, at which point you will be subject to taxes and penalties.

So, according to Haakons, you need to think about your investment timeframe and priorities. Bitcoin’s value could skyrocket tomorrow, but it will not help you if you are decades away from retirement. If you are thinking of a short-term investment, a brokerage account with more buying and selling flexibility might be a better choice.

It is also important to understand where you are investing your money. Dan Kemp, Chief Investment Officer of Morningstar Investment Management, recently cautioned against buying bitcoin or any digital currency just because it is what your friends are talking about.

Understand the differences between crypto-assets and bitcoin, and why they are seen as superior long-term prospects by some investors. Also, keep in mind that there is always some hot new investment that promises to turn the average person into a millionaire quickly. But, practically, things are not always so easy.

According to Haakons, investing in safe bets like index funds, and committing only 5% of your portfolio to bitcoin wagers are not always a bad idea. It all boils down to how much you are willing to take a chance. You should only invest money you can afford to lose in something unproven like bitcoin or other cryptocurrencies.

Haakons commented that it will not be a massive risk if you keep it to the maximum of 5% of your retirement savings unless you have a lot of money in there. You will still have a strong foundation thanks to mutual funds and exchange-traded funds (ETFs). an investment that promises to turn the regular individual into a millionaire quickly. But, practically, things are not so easy after all.

How Much Is It Worth to Invest in Bitcoin IRAs?

The Internal Revenue Service (IRS) does not have a cryptocurrency-specific account. As a result, when investors talk about ‘Bitcoin IRA’, they’re referring to an IRA that contains bitcoin or other digital currency within its holdings.

A self-directed IRA is sometimes known as a Bitcoin IRA. Self-directed individual retirement accounts (SDIRAs) allow you to invest in assets such as real estate, precious metals and cryptocurrency that are not allowed in traditional IRAs.

Suggested articles

FMTV Interview: Marketing in FintechGo to article >>

Investing in Bitcoin for retirement may increase your investment returns and diversify your portfolio, but it also adds a significant amount of risk to your retirement portfolio. If you are self-employed or operate a small business, SEP and Simple IRAs, as well as solo 401(k)s, offer significantly larger contribution limits.

Additionally, you can transfer money from a traditional IRA to a self-directed IRA. The IRS has treated bitcoin and other cryptocurrencies in retirement plans as property since 2014, which means coins are taxed similarly to equities and bonds.

According to the Retirement Industry Trust Association (RITA), between 2 and 5% of all IRAs are currently invested in alternative assets.

You will need to keep three things in mind:

Your IRA is held by a custodian, who handles its safekeeping as well as ensuring that your account complies with IRS and government rules. With traditional IRAs, banks and other financial entities often fulfil this function.

Your cryptocurrency trades are managed by an exchange. A crypto exchange (sometimes referred to as a DCE or digital currency exchange) is equivalent to a stock exchange. It is a marketplace for digital currencies, and it is where you will get your Bitcoin, Ethereum, or any cryptocurrency.

Your cryptocurrency is safe with a secure storage solution. Most Bitcoin IRA providers feature patented secure storage mechanisms to help protect your digital assets from theft after you buy them.

A custodian is required for IRA participants who want to include digital tokens in their retirement funds. Many investors have discovered that finding a custodian who accepts bitcoin in an IRA might be difficult. Custodians and other companies that let investors include bitcoin in their IRAs have grown in popularity recently.

Self-directed IRAs (SDIRAs) are increasingly allowing for alternative assets like cryptocurrencies, which is beneficial for consumers who want to include bitcoin in their IRAs. Some of the early leaders in this area are companies like BitIRA, Equity Trust, and Bitcoin IRA.

Let’s analyze the pros and cons of Bitcoin IRA:

Pros:

Tax benefits – Tracking trades and calculating taxes owed is the single biggest problem for Bitcoin investors. Because you owe taxes every time you sell cryptocurrencies for a profit, keeping track of multiple purchase prices and gains can be an accounting problem. Investing in a tax-advantaged account, such as a regular or Roth IRA, relieves this burden because it does not tax you on anything as long as the funds and assets remain in the account. Furthermore, you will benefit from the compounding growth of value that you will not lose due to taxes.

High-return potential – Bitcoin is extremely volatile, yet with volatility comes the potential for massive gains. For example, the value of Bitcoin was at $5,200 on March 15, 2020, and completed the year at $30,000, while Ethereum, the second most popular cryptocurrency, increased by almost 400% in 2020. Bitcoin’s massive potential is definitely worth the risk, especially if you are only investing a small portion of your IRA’s total value.

Diversification – Cryptocurrency is an asset class that is different from stocks and bonds, which are the most commonly held assets in retirement accounts in the United States. Even while crypto is risky in its own way, this could help secure your retirement funds.

Cons:

Volatility – The price of Bitcoin has fluctuated from close to $20,000 in December 2017 to as low as $3,400 in December 2018. Such volatility poses significant danger to an IRA, particularly for those nearing retirement.

Fees – Unlike traditional IRAs, self-directed IRAs usually have a higher charge structure. Make sure you understand all the charges associated with investing in cryptocurrency for retirement, from setup fees to trading and account administration fees.

Exchange restrictions – Some Bitcoin IRA providers will only let you trade on affiliated currency exchanges. Others provide you with the option of selecting your favorite exchange. If you want to invest with a certain crypto exchange, make sure your Bitcoin IRA provider enables it.

Complexity – When you invest in a Bitcoin IRA, you will almost certainly need to maintain at least one additional retirement account in addition to dealing with the moving parts of custodians, exchanges and secure storage. This is because Bitcoin IRAs are not set up to allow traditional assets like equities, bonds and mutual funds. This can make retirement planning even more difficult.

Final Takeaway – Should You Include Bitcoin in Your Retirement Portfolio?

Diversification is an important factor. Bitcoin is a very volatile investment, but some industry professionals believe it is an excellent one to have in your portfolio.

Before including it, though, you must be aware of the risk. Consult your financial advisor about the percentage of your portfolio that you should allocate to Bitcoin.

Bitcoin’s price decreased by about 85% between December 2017 and December 2018. However, it has increased tenfold since that low point, showing that volatility cuts both ways.

The higher the volatility of an investment, the higher the losses, but it also increases the potential gains. Whatever amount you invest, make sure you do your homework by understanding not only digital currencies but also the blockchain technology that powers them.

If you decide to invest in Bitcoin, be sure you are in it for the long haul and that you know you could lose all of your money. This is what experts refer to as an ‘acceptable loss’.

You do not have to buy coins directly because there are crypto-focused mutual funds. You should not invest in these types of assets if you do not understand how premiums and discounts work. Also, keep in mind the tax implications for this form of investment in the funds where you put it.

Given the volatility of cryptocurrencies, it is probably not the best idea for individuals closer to retirement to incorporate Bitcoin in their portfolio. On the other hand, those with a longer time frame and a higher risk tolerance may find that investing a modest portion of their retirement savings in alternative assets, such as Bitcoin or other cryptos, might provide an upside and protect them from losses in their traditional holdings.

Make sure you understand the fees structure before investing. Lastly, and perhaps most significantly, consider using Bitcoin and other cryptocurrencies as a minor portion of your total retirement plan, rather than the entire strategy.

Lyle Solomon serves as a principal attorney for the Oak View Law Group in Los Altos, California.

From the earliest days I built Coinbase to harness the power of cryptocurrency and create more freedom in the world. Five years ago we codified this into the first version of our vision, mission and strategy, the top level objectives that our products and goals align to.

Every few years we take another look and see if we can improve the communication of these core tenets. Why? Because they inform almost every decision we make at Coinbase. “Does this help us achieve our mission?” is one of the most common questions we ask ourselves. This is how we ensure the decisions we make and products we ship are helping to drive our mission forward.

One of my philosophies around building a company is that you have the opportunity to stick only a few key messages in people’s heads about what you’re trying to achieve in the world. There are too many other brands in the world for people to remember much more than that. In this vein, we recently rolled out a simplified set of artifacts that describe Coinbase, with the goal of distilling each to their core.

Here is how we define them:

Our Mission: What we’re trying to achieve in the world

Our Strategy: How we are going to get there

Our Culture: How we hire and work together

If people only remember one item, it should be our mission.

Mission

Our mission is to increase economic freedom in the world.

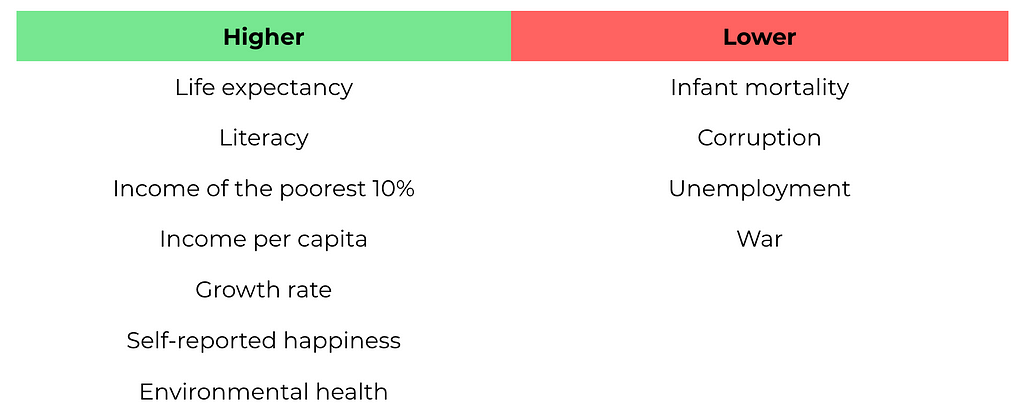

Why economic freedom? Economic freedom is a global indicator that is clearly defined and has been measured for decades. It is a composite metric, assessed both globally and for every country, that looks at a variety of factors like property rights, stability of currency, ability to start the business you want and work where you want, free trade, corruption, etc.

Economic freedom is a necessary, if not sufficient, condition for human progress. Societies with greater economic freedom have higher life expectancy and GDP growth, less war and corruption, better treatment of the environment, and higher income of their poorest 10%. Higher economic freedom correlates with the kind of societies that we all aspire to create.

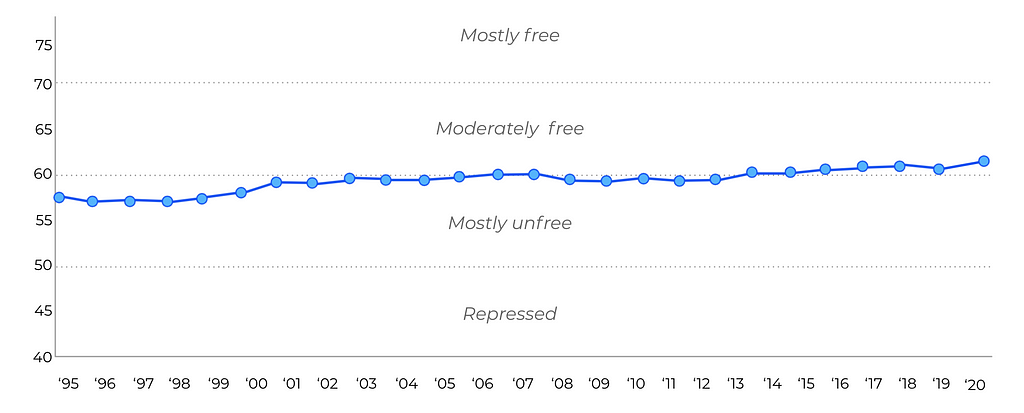

The problem is that economic freedom isn’t growing fast enough; the trend over the last 25 years has been a very gradual increase. Our job at Coinbase is to bend the shape of this curve upward.

Index of Economic Freedom (Heritage Foundation)

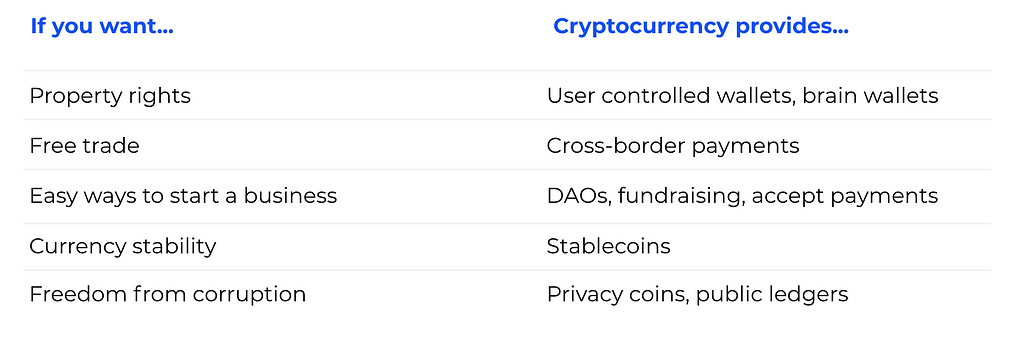

When I first read the Bitcoin whitepaper back in 2010, I realized this computer science breakthrough might be the key to creating more economic freedom. The current financial system is rife with high fees, delays, unequal access, and barriers to innovation. In many countries, citizens don’t have access to sound money, a functioning credit system, or even basic property rights. I realized that we could use cryptocurrency to create sound financial infrastructure in every country around the world.

Cryptocurrency can provide the core tenets of economic freedom to anyone: property rights, sound money, free trade, and the ability to work how and where they want.

At Coinbase, we are laser focused on increasing economic freedom, because we believe that this is how we can have the biggest impact on the world. Everyone deserves access to financial services that can help empower them to create a better life for themselves and their families, and Coinbase is tasked with making this future a reality.

Strategy

About five years ago, I wrote the Coinbase Secret Master Plan that outlined the four phases I envisioned cryptocurrency going through on its path to reaching 1 billion users. We have made incredible progress towards this plan, with >50M verified users on Coinbase, and more using other crypto products.

If our mission of increasing economic freedom is what we’re trying to achieve, then our strategy represents how we’re going to get there. This revised framing reflects where we are in the evolution of crypto 5 years later, and what we think the next 5+ years will look like.

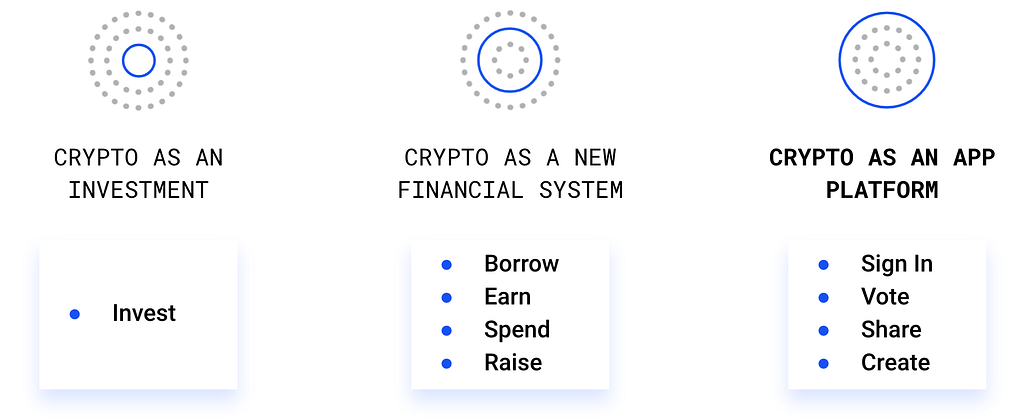

Our strategy has 3 pillars:

CRYPTO AS AN INVESTMENT

Crypto investing remains our core business and it’s the foundation of growing the cryptoeconomy. Investing is the first use case for every crypto holder and user, and we are the world’s most trusted onramp. We will continue focusing on:

Adding new assets: Ramp pace of asset addition, ultimately offering every reputable cryptocurrency to our users (read: not a scam, or illegal).

Institutional infrastructure: Building advanced trading tools professional traders are used to in traditional markets; building out the critical infrastructure and prime brokerage services to bring access to crypto markets to institutions of all sizes.

International expansion: Grow the reach of crypto, enabling safe and easy to use onramps in every country we can legally operate.

CRYPTO AS A NEW FINANCIAL SYSTEM

Crypto investing was the first use case, and it is bootstrapping a large and growing network of crypto holders. As more users hold crypto, new products will be built to help them use their crypto. Coinbase will offer financial services that are powered by modern crypto infrastructure, including:

DeFi: Safe and easy-to-use onramp to emerging decentralized finance use cases, accessible from the Coinbase app.

Payments: Tools to send and receive fast, cheap, and global payments, as well as tools for any merchants or businesses to accept crypto.

Earning: Unique opportunities to make money in crypto native ways, including staking (participating in network governance) and airdrops for completing educational tasks and incentives.

Borrowing/lending: More open, and more fair access to credit, as well as additional opportunities to earn yield on assets.

Our centralized products will continue to play a critical role in the growth of the cryptoeconomy. Over time, we expect DeFi (decentralized finance, built on open protocols) to outpace CeFi (centralized finance, including first party Coinbase products). We embrace decentralization, and will build products to make interacting with new DeFi as easy as we do our own first party products.

CRYPTO AS AN APP PLATFORM

Finally, crypto companies and protocol teams are driving new innovations and products beyond financial use cases. Coinbase will invest deeply in discoverability and usability of third party products in the cryptoeconomy, and make crypto as easy to use as it is to buy:

Surfacing apps: Enable our users to discover new applications and networks in our core product.

Externalizing shared services: Externalize our robust crypto infrastructure to non-crypto native organizations, making it safe and easy for anyone to interface with the cryptoeconomy.

Investing in the cryptoeconomy: Provide financial support for new compelling projects and teams through Coinbase Ventures that we think can help increase crypto adoption or otherwise further our mission.

Culture

Our mission and strategy are the what and the how, but building a world class company starts with building a high performing team. Our #1 priority is attracting and retaining top talent, which is why we are constantly working to build a culture to enable our team to do the best work of their careers. Our culture is the foundation of how we hire, and promote, and we’ve described it in detail in this document.

If you’re passionate about our mission, strategy and culture, come help us build the cryptoeconomy.

Our Mission, Strategy and Culture was originally published in The Coinbase Blog on Medium, where people are continuing the conversation by highlighting and responding to this story.