Singapore, 14th March 2022 — Decentralized cross-chain lending platform Fountain Protocol has launched a liquidity mining program on the Oasis mainnet, attracting over $15 million in TVL (total value locked) within 24 hours.

The strong launch earns Fountain Protocol a third-place ranking as compared to all other protocols on the…

Examining crypto’s usage in Ukraine, sanctions, and the Biden Executive Order

Around the Block from Coinbase Ventures sheds light on key trends in crypto. Written by Connor Dempsey

There’s a gravitational shift taking place within our industry. Since Russia’s shocking invasion of Ukraine, crypto has been:

used to crowdfund tens of millions for the Ukrainian defense

incorrectly speculated as a viable avenue for the Russian government to evade sanctions

the focus of a historic Executive Order put forward by the Biden administration

At this point, one thing is clear: this technology is a major emerging force in the geopolitical landscape. In this edition of Around The Block, we examine crypto in a geopolitical context, along with the difficult questions the world is asking.

An email address for money

In the aftermath of Russia’s attack on Ukraine, crypto’s power for coordinating economic activity was put on full display once the official Ukrainian twitter account tweeted out a plea for aid, accompanied with two long strings of letters and digits.

These long strings of characters were the Bitcoin and Ethereum addresses of the Ukrainian government, and the tweet represents the first time a nation state has ever sought aid directly in crypto. At a time when the Ukrainian government and banking sites were being flooded with DDoS (denial of service) attacks, and crowdfunding platforms were deplatforming organizations raising aid for Ukraine, the utility of permissionless, borderless networks for sending money was vividly illustrated.

At this time of writing, the Ukrainian government has collected over $50M in Bitcoin, ETH, ERC-20 stablecoins, and in other assets like DOT, DAI, and even Dogecoin.

The Ukrainian government has said that it has been using the funds to buy military supplies including bullet-proof vests, drones, gasoline, and night vision goggles. What’s more interesting is that 40% of suppliers have accepted payment in crypto.

Many have pointed out the oddity of private citizens from around the world essentially crowdfunding a war effort. Yet another sign of just how unprecedented all of this is.

NFTs enter the fold

Fungible crypto assets weren’t the only donations to pour into the Ukrainian government’s crypto wallet. NFT enthusiasts also answered the call, donating over 200 pieces of digital art work and even ENS addresses. Most notably, a rare CryptoPunk worth an estimated $200,000 was donated.

What’s interesting is that since the ownership provenance of the CryptoPunk will forever be associated with the defense of Ukraine, this added historical significance could raise its value over the long term.

The NFT aid didn’t stop there, as they were also combined with another crypto primitive to support the defense of Ukraine: DAOs.

UkraineDAO

Decentralized autonomous organizations were cast into the limelight last year after ConstitutionDAO crowdsourced $40M in under a week in a bid to buy one of the original copies of the US Constitution. While the bid ultimately failed, it underscored the power that these software enabled organizations have for coordinating economic activity at the speed of the internet.

After a Ukrainian NGO (non-government organization) supporting the war effort called Come Back Alive was de-platformed from crowdfunding platform Patreon for supporting military activity, they also turned to crypto. Shortly thereafter, UkraineDAO was created to help support this NGO.

The DAO minted a 1:1 NFT of the Ukrainian flag and put it up on PartyBid, which allows groups to pool funds to buy NFTs. In essence, the DAO created its own NFT, crowdsourced as much money as they could to buy it from themselves and then donated the proceeds to Come Back Alive. All told, they raised $6.7M. They also distributed commemorative “valueless” tokens called LOVE to those who donated.

Crypto on the main stage

Between the Ukrainian government and various NGOs, over $80M and counting in aid has been raised. While in the grand scheme of things this amount is a nominal sum not likely to turn the tides of war, it’s also far from insignificant. The sum represents over 20% of the $350M pledged by the Biden administration and is a powerful display of the promise that decentralized, borderless money holds.

Slowmist, where we’re pulling this data, also noted that when you factor in other organizations and cryptocurrencies they’re not tracking, the full figure is likely over $100M. The Giving Block, for example, raised over $2.3M in crypto donations for over 20 non-profits supporting Ukrainian relief.

Beyond support of the Ukrainian government and organizations, crypto has also proven useful for individual Ukrainians affected by the crisis. One Ukrainian who fled to Kazakhstan reported that he lost access to his savings and that his credit cards were no longer functioning, leaving crypto as his only financial life raft: yet another example of the utility of permissionless finance.

At their core, Bitcoin, Ethereum, and the like are neutral technologies that anyone with an internet connection can use. While we celebrate the use of these neutral technologies to help a nation defend itself against a foreign invader and as a lifeline for refugees, it also begs the question: what about their use by those on the other side of the conflict? Principally, the Russian government.

The burning question

Western governments responded to Russian aggression with unprecedented sanctions against the Russian government. This coincided with widespread narratives surrounding the potential for cryptocurrencies to be used to circumvent those very sanctions.

Before we examine the fact or fiction behind these claims, it helps to understand what these sanctions entail.

Russian sanctions

Since Russia invaded Ukraine, governments around the world, including the U.S., have imposed sanctions targeting the Central Bank of Russia, major Russian commercial banks and companies, Vladimir Putin, Russian elites, among others. In aggregate, these sanctions cut targeted individuals and entities off from international banking and in many instances, freezes their assets.

Among the most substantial sanctions imposed was kicking major Russian banks out of SWIFT, which is the financial network used by over 11,000 banks and institutions to move trillions of dollars across borders. This severely limits Russia’s ability to receive payments for oil and gas: their main export. For context, when Iranian banks were banned from SWIFT in 2012, and sanctions were imposed on Iranian oil purchasers, Iran lost nearly half of its oil export revenue and 30% of its foreign trade.

The most drastic sanction is from the US, UK, and EU banning transactions with the Russian Central Bank. The Russian Central Bank holds roughly $630B in the form of the world’s major reserve currencies — the dollar, euro, pound, yuan — as well as 2,300 tons of gold. With this sanction, Russia suddenly has no one to sell its reserves to, rendering its entire stockpile useless.

Is crypto their answer?

We’ve seen public speculation on how crypto could be used to evade those sanctions. However, that speculation has been unfounded as the crypto market is simply not large enough to help Russia meaningfully circumvent them.

Consider the Russian Central Bank’s $630B in immobilized assets. That’s 80% of Bitcoin’s market cap and larger than the rest of the crypto market put together. Converting that much fiat into crypto would take 5–10x the total daily traded volume of all digital assets, so the liquidity just isn’t there.

Additionally, as our Chief Legal Officer previously pointed out, trying to obscure large transactions using open and transparent crypto technology would be far more difficult than other established methods (e.g., using fiat, art, gold, or other assets).

The Biden Executive Order

As crypto played a significant role in the defense of Ukraine, it was also cast into the fore of the American political system. Late last week, the Biden Administration published its long awaited Executive Order on digital asset regulation.

The Executive Order simply directed federal agencies to study the benefits and risks of digital assets, as opposed to putting any immediate legislation into action. On one hand, many were pleasantly surprised with the optimistic tone of the EO, as it acknowledged crypto and Web3 technologies as critical for the future of U.S. national economic competitiveness. On the other, the report focused more on the potential risks of crypto rather than its societal benefits.

The EO calls on a total of 23 federal government agencies, organizations, and White House Offices to assemble huge reports on the risks stemming from crypto. This outsized focus on risk, when compared to past EOs, has caused some people to worry that the Biden Administration doesn’t fully recognize the power and potential of digital assets, even as that power is being plainly demonstrated on the world stage.

While the EO may have felt like a milestone, it is ultimately the start of a long road ahead. One in which the whole of the US government will finally seek to fully understand the importance of this technology. It is critical that the government fully explores not only the risks, but also the benefits that digital assets bring, with enough transparency to allow the public to weigh-in on a federal approach to regulation.

Ultimately, this presents a tremendous opportunity for the industry to engage with regulators about how to best embrace the transformational nature of crypto and Web3 technologies.

Closing thought

To sum it all up, regardless of how you feel about crypto’s application in funding a war effort or the increased attention it’s receiving from the most powerful government in the world, it’s apparent that we’ve entered uncharted territory: this next phase of crypto adoption will look drastically different from the last.

ATB Podcast: Crypto’s Role in the Ukraine Crisis with Elliptic’s Dr. Tom Robinson

By Prakash Hariramani, Senior Director, Product Management, and Bipul Sinha, Senior Product Manager

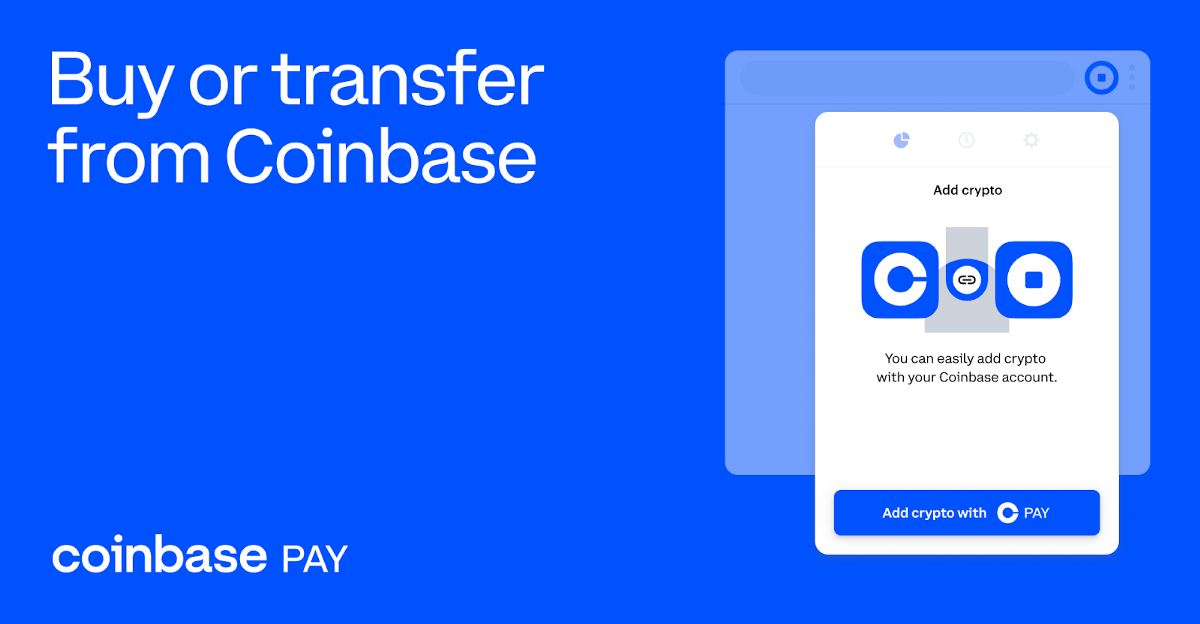

Today, we are introducing Coinbase Pay, the easiest way for Coinbase users to fund their Coinbase Wallet from the Chrome browser extension and explore web3.

Over the past year, DeFi, NFTs, and other web3 services have seen tremendous adoption. However, a key step in being able to access and use these services — funding a self-custody wallet — is a cumbersome process that involves multiple steps, switching between apps, and manual transfers.

Coinbase Pay eliminates these steps, and makes it easy and intuitive for anyone to participate in DeFi or purchase NFTs, in just a few clicks.

Cash. Click. Crypto.

Before Coinbase Pay, users who wanted to add funds to their Coinbase Wallet from the browser extension needed to navigate to Coinbase.com, sign in to their account, copy-paste their wallet address, and manually transfer funds from their Coinbase account.

The process was not only cumbersome, but also left the user vulnerable to user error. For example, if funds were accidentally sent to the wrong wallet address, they would be irretrievable.

Coinbase Pay makes the process faster, easier, and more secure than ever before. All you need to do is select “Add crypto with Coinbase Pay” when you want to add crypto to your Coinbase Wallet extension.

Next, you simply select the currency you want to add to your wallet, specify the amount, confirm the transaction–and that’s it. No more switching between apps, copy-pasting addresses, and manually transferring funds.

Coinbase users based in the US and Canada can currently use their debit cards and bank accounts for transfers, with more payment options enabled globally soon.

First-time users of Coinbase Wallet will need to link their self-custody wallet to their Coinbase account before being able to use Coinbase Pay.

Making it even easier to access the world of DeFi, NFTs, and more

At Coinbase, our mission is to increase economic freedom in the world. A key part of realizing this mission is building crypto products and services that are easy-to-use and accessible. Coinbase Pay makes it even easier for users to get web3-ready with Coinbase Wallet.

With the Coinbase Wallet extension, your Chrome browser can securely interact and engage with all manner of web3 applications. Kickstart your NFT collection, earn yield through DeFi lending protocols, and grow your crypto portfolio with hundreds of thousands of tokens supported via decentralized exchanges (DEXes).

And now you can engage with dapps with greater peace of mind, knowing that your payment credentials remain safely stored within Coinbase.

Looking forward

We are continuing to build new features into Coinbase Wallet to make it the most user-friendly and accessible self-custody wallet in the world, making it easier for more users to enter the world of web3. We will also continue to expand Coinbase Pay to bring the benefits of seamless fiat onramp to the crypto ecosystem. Stay tuned for more updates.

Make sure to follow us on Twitter for the latest news about Coinbase Wallet and Coinbase Pay.

Coinbase Wallet is a self-custody wallet providing software services subject to Coinbase Wallet Terms of Service and Privacy Policy. Coinbase Wallet is distinct from Coinbase.com, and private keys for Coinbase Wallet are stored directly by the user and not by Coinbase. Fees may apply. You do not need a Coinbase.com account to use Coinbase Wallet.

Dubai, U.A.E., March 10, 2022 — MRHB DeFi Network, the world’s first decentralized finance (DeFi) platform focused solely on providing ethical and halal crypto opportunities, is listing its $MRHB token on BitMart, a global centralized cryptocurrency exchange (CEX). This follows its current listing on LBank Global Exchange as well as popular DEX, Pancakeswap.

Expand your dapp’s reach with just a few lines of code

By Sid Coelho-Prabhu, Product Management Director, Wallet

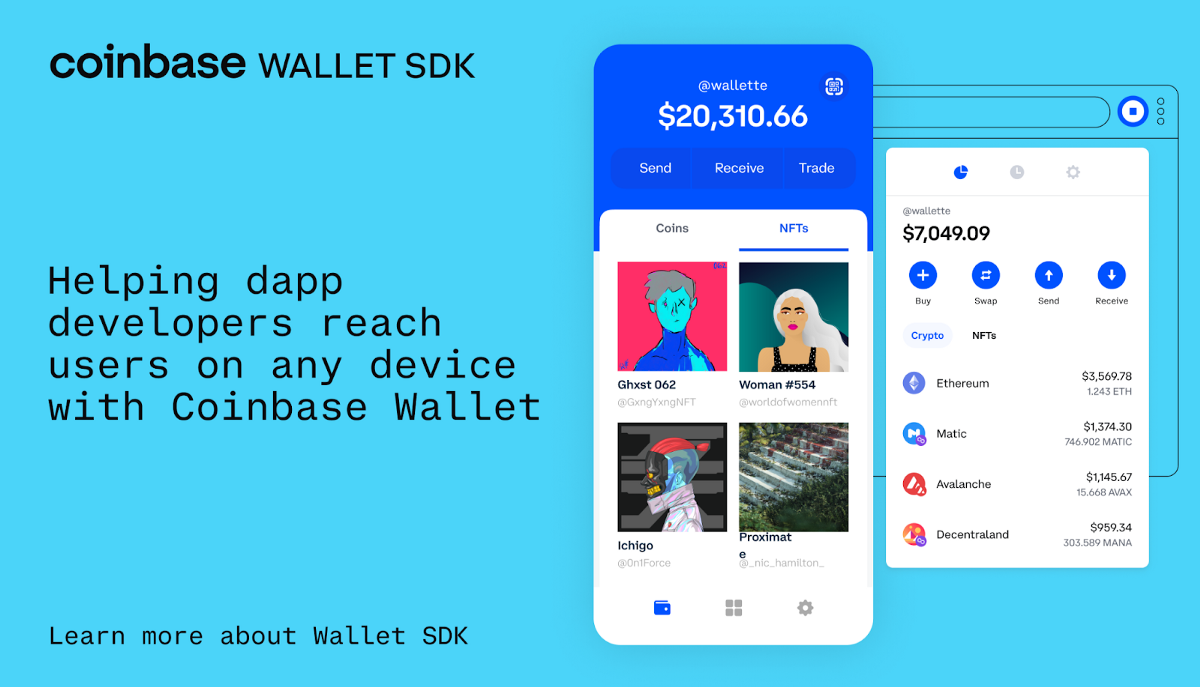

Millions of people choose Coinbase Wallet to use dapps, earn yield with DeFi, trade more than hundreds of thousands of assets, and hold their NFTs. In just minutes you can integrate Coinbase Wallet in your dapp, expanding your reach to users on all of their devices — and open your dapp up to the multichain Coinbase ecosystem of over 89M users across 85 countries, on whatever device they prefer.

With just a few lines of code, you can open up access to your dapp to Coinbase Wallet users across the iOS and Android mobile apps as well as the Wallet browser extension on Chrome.

Coinbase Wallet SDK takes just 5 minutes to integrate and doesn’t require you to deploy any additional infrastructure. You can learn how to integrate with Coinbase Wallet in our technical documentation, read our post on using web3-react to connect, or watch the Coinbase Wallet SDK demo.

We are dedicated to making the benefits of crypto and the entire web3 ecosystem accessible to all — regardless of network or blockchain, country or currency, crypto savvy or crypto skeptical. We’re building Coinbase Wallet to reflect that commitment. With support for all EVM-compatible chains, including Avalanche, BNB Chain, Polygon, and many more, you can access millions of users for your dapp across the most popular ecosystems.

We also know that security is top-of-mind for anyone building in the web3 ecosystem. By offering integration with the most trusted and secure name in crypto, you can help put your users at ease while they explore your dapp, confident that their crypto and data are safe.

The built-in trust offered by Coinbase Wallet shows: As of February 2022 it’s the most downloaded mobile dapp wallet in the United States. Integrating your dapp with Coinbase Wallet can immediately unlock access to 12M Wallet users, with the potential to reach the full Coinbase ecosystem of over 89M users in 85 countries.

We see Coinbase Wallet SDK as a critical way to expand access to dapps, which is why we want this experience to be available to everyone in the crypto community. To make that possible, Coinbase Wallet SDK is open-source, making it available for any dapp developer that wants to integrate it into their product.

Crypto is just getting started, and Coinbase Wallet is your key to what’s next. For developers, Coinbase Wallet is the best self-custody wallet to integrate with, as it’s the most trusted name in crypto and offers unparalleled reach to 89M users across the entire Coinbase ecosystem. Coinbase Wallet also offers the most user-friendly self-custody experience, unlocking the entire world of crypto, including collecting NFTs, earning yield on your crypto, accessing play-to-earn games, engaging in DeFi, participating in DAOs, and more. To learn more, visit our website.

Disclaimer:

Coinbase Wallet is a self-custody wallet providing software services subject to Coinbase Wallet Terms of Service and Privacy Policy. Coinbase Wallet is distinct from Coinbase.com, and private keys for Coinbase Wallet are stored directly by the user and not by Coinbase. Fees may apply. You do not need a Coinbase.com account to use Coinbase Wallet.

We started our journey in 2012 by offering the safest and easiest platform to buy and sell Bitcoin. Fast forward to 2022, and we now offer over 150 tradable assets and our customers still enjoy Coinbase as the safest and easiest platform to use. But, this is just the beginning. Today, we’re excited to share some of our efforts to bring you more transparency and information for newly tradable assets, and how we’re introducing more tools and protections to elevate your trading experience on Coinbase.

More transparency and information than ever

As we expand our asset offerings, we will be bringing on more, often newly created assets or lesser known tokens that could come with additional trading risks, including higher price swings and increased order cancellations.

Our goal is to be as transparent as possible with our customers regarding trading risks, so we are introducing a new experimental label on asset pages and a disclosure when executing trades for some assets. Customers will now begin noticing this label and other transparency initiatives across Coinbase today. Learn more about experimental assets in our Help Center.

At Coinbase, your trust is our top priority. We want to help you trade more assets while keeping your account protected. We’re aiming to add even more assets and expand our coverage around the globe in the coming months, so stay tuned for more updates.

Coinbase is committed to building a safe and responsible financial system that promotes economic freedom around the world. We strive to be the most trusted platform for buying, selling, and exchanging digital assets, helping everyday people to participate in the crypto economy. We earn that trust by working hard to ensure the integrity of all transactions supported by our platform, and a critical part of that goal is our compliance with economic sanctions.

Coinbase is committed to complying with sanctions

In the past few weeks, governments around the world have imposed a range of sanctions on individuals and territories in response to Russia’s invasion of Ukraine. Sanctions play a vital role in promoting national security and deterring unlawful aggression, and Coinbase fully supports these efforts by government authorities.Sanctions are serious interventions, and governments are best placed to decide when, where, and how to apply them.

No compliance program is perfect, including ours. But to play our part in these critical economic sanctions, Coinbase implements a multi-layered, global sanctions program. We take steps to:

Block access to sanctioned actors. During onboarding, Coinbase checks account applications against lists of sanctioned individuals or entities, including those maintained by the United States, United Kingdom, European Union, United Nations, Singapore, Canada, and Japan. To open a Coinbase account, individuals and entities must provide identifying information, including their name and country of residence. We screen this information via an independent vendor before permitting an individual to transact. If a customer lives in a sanctioned country or region, or if they are identified as a sanctioned individual or entity, they cannot open an account on our platform. Similarly, we use geofencing controls to prevent access to the Coinbase website, as well as our products and services, by anyone using an IP address in a sanctioned geography (e.g., Crimea, North Korea, Syria, and Iran). We routinely subject our sanctions compliance program to internal testing and independent audits by third-parties.

Detect attempts at evasion. Coinbase regularly updates the global sanctions lists that we use for screening. If someone has opened a Coinbase account and is later sanctioned, we use this ongoing screening process to identify that account and terminate it. Because sanctions evaders often try to mask their identities, Coinbase also proactively works to map transactions beyond the entities and individuals specifically flagged by governments. This allows us to identify potentially related parties and block accounts associated with prohibited actors.

Anticipate threats. Coinbase maintains a sophisticated blockchain analytics program to identify high-risk behavior, study emerging threats, and develop new mitigations. For example, we have methods for identifying accounts held by sanctioned individuals outside of Coinbase, even if we don’t have direct access to their personal information. For example, when the United States sanctioned a Russian national in 2020, it specifically listed three associated blockchain addresses. Through advanced blockchain analysis, we proactively identified over 1,200 additional addresses potentially associated with the sanctioned individual, which we added to our internal blocklist. This is just one example. Today, Coinbase blocks over 25,000 addresses related to Russian individuals or entities we believe to be engaging in illicit activity, many of which we have identified through our own proactive investigations (Note: this figure isn’t specific to the time period since the invasion of Ukraine, most of these addresses we identified prior to the invasion, and we have not seen a surge in sanctions evasion activity in the post-invasion context). Once we identified these addresses, we shared them with the government to further support sanctions enforcement.

The benefits of digital assets for sanctions enforcement extend beyond these initiatives. Digital assets have properties that naturally deter common approaches to sanctions evasion.

Ordinary fiat currency laundered through traditional financial institutions remains one of the most common mechanisms for sanctions evasion and money laundering. As the United States Treasury noted of sanctions against Iran, the “Iranian regime has long used front and shell companies to exploit financial systems around the world” to evade sanctions.

An entire money laundering industry has emerged to hide assets in ordinary fiat currency using these techniques. By transacting through shell companies, incorporating in known tax havens, and leveraging opaque ownership structures, bad actors continue to use fiat currency to obscure the movement of funds. In this way, they leave complex financial trails that are difficult to trace, requiring investigators to separately request information from many different financial institutions, and follow a trail across multiple countries (some of which refuse to cooperate or take years to produce records).

By contrast, digital asset transactions are traceable, permanent, and public. As a result, digital assets can actually enhance our ability to detect and deter evasion compared to the traditional financial system.

Public. Public blockchains offer unprecedented visibility into the details of transactions, including information about the date and time of each transaction, the type of virtual asset transacted, the amount, the wallet addresses involved, and the unique transaction identifier. Suspicious transaction activity can be traced without needing to gather information from multiple financial institutions. These advantages for investigation and enforcement simply do not exist with cash transactions or transactions across multiple countries.

Traceable. When applied to public blockchain data, analytics tools offer law enforcement additional capabilities. In many cases, law enforcement can trace the transaction history of a wallet from the very first transaction, follow transactions in real time, and group transactions according to risk level based on interactions with other wallets. Other techniques can help authorities to follow transactions between chains or through intermediaries. For example, Coinbase’s proactive on-chain analysis identified more than 16,000 addresses possibly associated with Iranian exchanges, many of which had not yet been identified by others. We used this analysis to strengthen our compliance systems and inform law enforcement in order to enhance industry-wide awareness.

Permanent. Once recorded on the blockchain, transactions remain immutable. No one (not crypto companies, not governments, not even bad actors) can destroy, alter, or withhold information to evade detection.

In addition to these technical advantages, adoption of digital assets is still nascent, making their use for widespread sanctions evasion — the kind that robs sanctions of their impact — unlikely, a fact recently noted by a national security expert.

For example, the Russian government and other sanctioned actors would need virtually unobtainable amounts of digital assets to meaningfully counteract current sanctions. The Russian central bank alone holds over $630 billion in largely immobilized reserve assets. That’s larger than the total market capitalization of all but one digital asset, and 5–10x the total daily traded volume of all digital assets. As a result, trying to obscure large transactions using open and transparent crypto technology would be far more difficult than other established methods (e.g., using fiat, art, gold, or other assets). This doesn’t mean that bad actors can’t try, but circumventing restrictions on this scale would require massive purchases that would be prohibitively expensive and detectable, as this buying activity would likely lead to price spikes.

We are always working to build trust in the crypto industry

These are just some of the ways that industry best practices and crypto technology help to support sanctions compliance. Of course, no traditional or crypto business can guarantee that its sanctions controls are completely airtight. Malicious individuals may find ways around even the strongest barriers.

The transparency of the blockchain is a formidable tool for law enforcement, and platforms like Coinbase work very hard to partner with law enforcement to root out bad actors. There is also a legitimate interest in protecting the privacy of individuals — a public policy principle long recognized in the traditional financial system. We believe we can balance these interests by continuing to support law enforcement efforts while promoting policy frameworks that respect individual privacy.

Coinbase helps everyday people to protect, build, and share their wealth through crypto technology. At the same time, we vigorously work to promote security, safety, and transparency on our platform, including through our commitment to sanctions compliance. We welcome public scrutiny of the crypto industry, and will continue working to enhance our overall compliance program and industry compliance standards. This is an integral part of our ongoing commitment to remaining the trusted platform that we, our customers, and the public expect.

MRHB DeFi recently announced a new strategic partnership with Sukhavati Labs, a decentralized cloud network service focused on storage. Now all NFTs minted on the MRHB DeFi network — such as on the SouqNFT Marketplace — will be stored in a secure and permissionless manner at a low cost on the decentralized Sukhavati network.

By Sonia Pinto, Senior Product Marketing Manager and Alexis Hamel, Product Manager, Custody

Coinbase Prime offers custody and trading for more than 50 DeFi coins and tokens, across a wide range of segments, including DEXs, lend, and borrow.We facilitate governance for a growing number of tokens including UNI, COMP, and MKR. This gives our customers the opportunity to directly participate in the governance of DeFi projects.

Asset managers, like Grayscale and Bitwise, are increasingly stepping into DeFi beyond Bitcoin and Ethereum. FinTechs are also expanding their DeFi offerings to cater to growing demand. Venture capital funding for blockchain startups reached $25 billion last year, up 713% from $3.1 billion in 2020. Coinbase Ventures, A16Z and Paradigm are some of the VCs doubling down on DeFi.

As one of the most trusted names in the industry, Coinbase offers access to a broad range of assets, customized account support, and a rapidly growing number of capabilities for our clients to participate in DeFi.

DeFi Opportunities

While Bitcoin or Ethereum are the currency of the blockchains, Defi tokens are built on top of the blockchain and represent a wide range of new opportunities for institutions. As of January 2022, nearly $200 Billion was deposited through smart contracts across major blockchains. This measure is referred to as the Total Value Locked (TVL). Ethereum-based projects alone account for 60% of DeFi TVL.

Defi offers a global, open alternative to financial services consumers utilize today — including savings, loans, trading, and insurance — creating a financial system that is automated, accessible 24/7, permissionless and more transparent. DeFi protocols with the highest adoption rates include Compound and Aave for lending, Curve for stablecoins swap, Uniswap for token swaps, or DYDX for derivatives.

Where do I start?

Gain access to our prime broker by navigating to coinbase.com/prime. Click “Get started” and fill in the required information to apply for a Coinbase Prime account. For our existing clients who have a Coinbase Custody, or Coinbase Exchange account, please contact your account manager or PrimeOps@coinbase.com.

The last time ETH Denver was held in person, ETH’s market cap stood at $30B, DeFi hadn’t had its breakout summer, and few people outside of the 6,000 attendees knew what an NFT was. Fast forward to 2022 and a 10x in ETH’s market cap, the rise of NFTs, a DAO resurgence, and a year where Ethereum did more transactional volume than Visa, a record crowd of 12,000 in Colorado were met with an entirely different energy.

What had historically been an event for hackers and coders received an infusion of artists and creatives, as well as a governor, a former presidential candidate, and a heavy dose of EDM — a reflection of Ethereum and crypto’s growing awareness within the mainstream.

Despite the new faces, ETH Denver retained its authentic quirky disposition, complete with bright neon colors and Vitalik dressed as a “Bufficorn”. Beyond a lone Doge Lambo, the main event was mostly free of flash and still felt authentically Ethereum.

Attendee sentiment

Even amidst a 50% market drawdown from late November highs and multi-hour long check-ins in the frigid cold, builder energy was sky high. Where Ethereum was still finding its footing during last ETH Denver, this year’s event featured heavy discussion across all of the new verticals thriving today: DeFi, NFTs, DAOs, gaming, and more.

It was also apparent just how much private capital is still flowing into crypto, undeterred by macro market headwinds: with seed stage deals raising at a minimum $50M and seed token rounds going for $100M+ (no shipped code needed), one might argue too much. In either case, it’s clearly a builders market.

Real Politik

In addition to investor and builder excitement, there was also a noticeable presence from mainstream politicians: most notably, Colorado Governor Jared Polis and the Forward Party’s Andrew Yang. With crypto and Web3’s growing popularity, it seems many in government are seeing the upside to embracing this emerging constituency.

In addition to posing with Vitalik, Gov. Polis announced during the conference that Colorado will accept crypto as payment for taxes in addition to making Colorado, “the first digital state” with favorable regulations for the crypto economy. This mirrors the positions of other crypto-forward governors like Miami’s Francis Suarez and New York’s Eric Adams.

Photo credit: Westword

In a surprise appearance, Andrew Yang took the stage with Bankless’s David Hoffman, sharing his thoughts on why Web3 represents “the biggest anti-povery opportunity of our time.” His appearance came on the heels of his Lobby3 initiative, which will advocate for thoughtful regulation in Washington to support crypto innovation.

All of the while, Biden’s executive order on crypto regulation loomed large (however if you bumped into CoinCenter’s Neeraj he would have told you that the EO is nothing to panic over). Either way, it’s clear that crypto has entered the fore of the American political discussion.

NFT Mania

Beyond the bullish builder sentiment, private investor froth, and political participation, NFTs were everywhere in Denver. NFT art installations, musicians performing with their NFTs on display, and some events even requiring NFTs to gain entry (shoutout ecodao).

POAP (Proof of Attendance Protocol) NFTs, which give people digital mementos commemorating attendance of a particular event by scanning a QR code, were particularly pervasive. The inventive ways different projects found to engage via POAPs suggests that they may be the next mainstream crypto community use case.

If you were mingling at any of the NFT centric events, odds are you bumped into a former FAANG employee newly entering the NFT space. A sign that despite the macro market downturn, NFT mania is still in full swing and the brain drain from Web2 to Web3 continues.

Signs of DAObt

Following a year that saw ConstitutionDAO capture global attention, DAOs have regained much of the crypto limelight. Conference booths were packed with projects building DAO infrastructure and discussions on how decentralized autonomous can rewire the world were prevalent.

While DAO enthusiasm was evident, many noted that DAO participants were starting to show signs of fatigue with many DAOs struggling to retain contributors. Joseph Delong, former CTO of SushiSwap who notably left the decentralized project, gave a memorable talk on why DAOs simply need more structure to be effective (also discussed in our recent podcast with Orca Protocol’s Julia Rosenberg).

With over 1B in startup equity for DAO tooling and under 200 DAOs, it begs the question: is there enough DAO to go around?

The long term outlook of DAOs seems to be bright, but the industry is still grappling with how exactly DAOs should function. Given that there’s no standardization around DAO operation, it’s hard to know what tools they actually need. As such, the DAO infrastructure sector will likely see a lot of turbulence over the near to medium term.

The Merge

After years in the making, experts stated that Ethereum’s transition to proof-of-stake is expected to happen in Q2 or Q3 this year. As a quick refresh, Ethereum’s PoS chain (the beacon chain) has been operational since December 2020, however all applications still live on the proof of work chain. The merge basically consists of migrating these applications to the PoS chain.

As such, the merge was a major point of discussion for devs this year. If all goes well, ETH holders won’t have to do anything, but developers and infrastructure providers are in preparation mode. This includes running testnets and conducting dry runs in anticipation for the real thing.

The Ethereum ecosystem is making a big bet on PoS in conjunction with layer 2 scaling solutions (rollups). In a post-merge world, Ethereum will transition to become a settlement layer for large transactions while most user activity is pushed to layer 2. This will create an environment where all EVM compatible layer 1s compete with ETH L2s for users and developer mindshare.

Also prepping for the merge, is Coinbase Cloud, which powers a portion of Coinbase’s ETH staking product as well as node infrastructure for many players in the space. Cloud developers showed up in force hosting a hackathon, a variety of panels, workshops, and a party for over 500 attendees. Learn more about how Coinbase Cloud is thinking about client diversity ahead of the merge here.

A builders market

In the days since ETH Denver wrapped, the market drawdown intensified as Russia escalated the situation in Ukraine. While crypto has rebounded, markets will likely remain shaky given the uncertainty of the current geopolitical situation. Regardless, teams building the next generation of Ethereum and Web3 remain well funded and the building will continue.

As evident by the increased diversity of both projects and participants at this year’s conference, what gets built on Ethereum will keep venturing out in a myriad of new exciting directions.