Ghana is working to develop offline capabilities for its forthcoming central bank digital currency (CBDC) in a bid to promote its use across all segments of Ghanan society.

According to a Oct. 18 report from Bloomberg, Kwame Oppong, head of fintech and innovation at the Bank of Ghana (BoG), revealed that the country’s digital currency “e-cedi” will support offline transactions during the Ghana Economic Forum on Monday.

Oppong emphasized that offline functionality will allow Ghanans who lack reliable access to electricity and internet connectivity to embrace the country’s CBDC, stating:

“The e-cedi would also be capable of being used in an offline environment through some smart cards.”

A smart card is a plastic credit card-sized card with a chip that allows its user to transact using a pre-loaded balance. A similar system has been trialled by Oxfam to facilitate payments using the decentralized stablecoin DAI to provide relief from environmental disaster.

According to World Bank data published during 2019, 84% of Ghanans then had stable access to electricity while just 53% were connected to the internet.

Related: G7 leaders issue central bank digital currency guidelines

During August, BoG announced it had partnered with German financial firm Giesecke+Devrient (G+D) to pilot a retail CBDC in Ghana.

The announcement came just one month after Ghanan vice president Dr. Mahamudu Bawumia advocated for African governments to embrace digital currencies as means to bolster trade across the continent during the Fifth Ghana International Trade and Finance Conference in July.

Local adoption of decentralized cryptocurrencies is also on the rise, with analytics firm Chainalysis reporting that Africa’s cryptocurrency market has grown by more than 1,200% since 2020 as of last month.

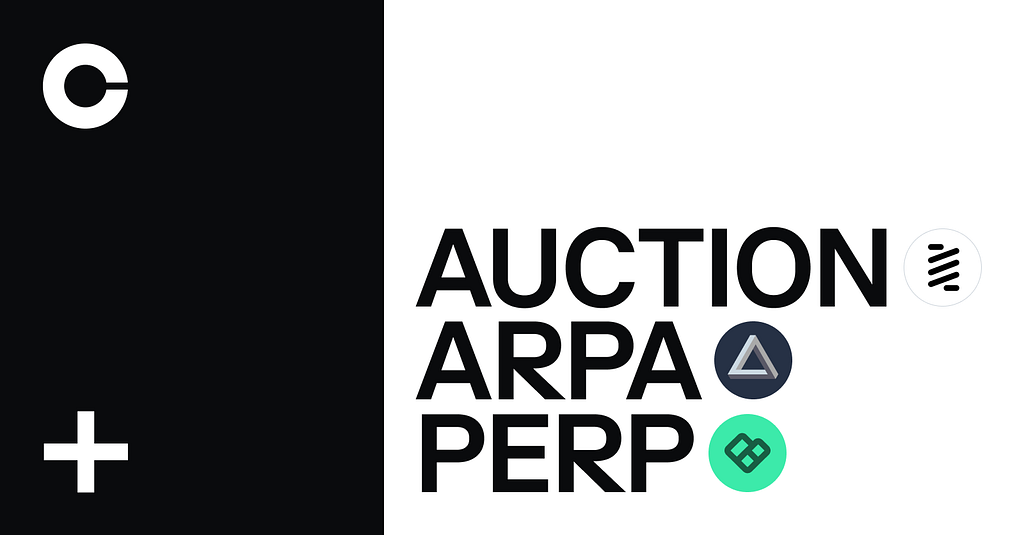

Starting Today, Monday October 18, transfer ARPA, AUCTION and PERP into your Coinbase Pro account ahead of trading. Support for ARPA, AUCTION and PERP will generally be available in Coinbase’s supported jurisdictions with certain exceptions as indicated in each asset page here. Trading will begin on or after 9AM Pacific Time (PT)Tuesday October 19, if liquidity conditions are met.

One of the most common requests we receive from customers is to be able to trade more assets on our platform. Per the terms of our listing process, we anticipate supporting more assets that meet our standards over time. Most recently we have added trading support for BadgerDAO (BADGER), Rarible (RARI), Function X (FX), Jasmy (JASMY), Wrapped Centrifuge (WCFG), Avalanche (AVAX), Adventure Gold (AGLD), Braintrust (BTRST), Rari Governance Token (RGT) XYO Network (XYO), DerivaDAO (DDX), DFI.money (YFII), Radicle (RAD), COTI (COTI) and Axie Infinity (AXS).

Starting Today, Monday October 18 we will begin accepting inbound transfers of ARPA, AUCTION and PERP to Coinbase Pro. Trading will begin on or after 9AM Pacific Time (PT) Tuesday October 19, if liquidity conditions are met.

Once sufficient supply of ARPA, AUCTION and PERP is established on the platform, trading on our ARPA-USD, ARPA-USDT, ARPA-EUR, AUCTION-USD, AUCTION-USDT, AUCTION-EUR, PERP-USD, PERP-USDT and PERP-EUR order books will launch in three phases, post-only, limit-only and full trading. If at any point one of the new order books does not meet our assessment for a healthy and orderly market, we may keep the book in one state for a longer period of time or suspend trading as per our Trading Rules.

We will publish tweets from our Coinbase Pro Twitter account as each order book moves through the phases.

Bounce (AUCTION) is an Ethereum token that powers Bounce, a decentralized auction protocol for token and NFT sales. AUCTION supports incentives on the protocol, provides benefits and governance rights for holders, and is used to pay for certified listings.

ARPA Chain (ARPA) is an Ethereum token that powers ARPA Chain, a computation network that enables privacy-preserving smart contracts, data storage, and scalable off-chain transactions. The ARPA token can be used to pay for data and computation in addition to governing the future of the network.

Perpetual Protocol (PERP) is an Ethereum token that powers Perpetual Protocol, a decentralized exchange for perpetual contracts. Using perpetual contracts, users can open leveraged long or short trading positions for a variety of assets.

ARPA, AUCTION and PERP are not yet available on Coinbase.com or via our Consumer mobile apps. We will make a separate announcement if and when this support is added.

You can sign up for a Coinbase Pro account here to start trading. For more information on trading ARPA, AUCTION and PERP on Coinbase Pro, visit our support page.

### Please note: Coinbase Ventures may be an investor in the crypto projects mentioned here, and additionally, Coinbase may hold such tokens on its balance sheet for operational purposes. A list of Coinbase Ventures investments is available at https://ventures.coinbase.com/. Coinbase intends to maintain its investment in these entities for the foreseeable future and maintains internal policies that address the timing of permissible disposition of any related digital assets, if applicable. All assets, regardless of whether Coinbase Ventures holds an investor or Coinbase holds for operational purposes, are subject to the same strict review guidelines and review process. This website contains links to third-party websites or other content for information purposes only (“Third-Party Sites”). The Third-Party Sites are not under the control of Coinbase, Inc., and its affiliates (“Coinbase”), and Coinbase is not responsible for the content of any Third-Party Site, including without limitation any link contained in a Third-Party Site, or any changes or updates to a Third-Party Site. Coinbase is not responsible for webcasting or any other form of transmission received from any Third-Party Site. Coinbase is providing these links to you only as a convenience, and the inclusion of any link does not imply endorsement, approval or recommendation by Coinbase of the site or any association with its operators.

Crypto is a new type of asset. Besides potential day to day or hour to hour volatility, each crypto asset has unique features. Make sure you research and understand individual assets before you transact.

All images provided herein are by Coinbase.

ARPA Chain (ARPA), Bounce (AUCTION) and Perpetual Protocol (PERP) are launching on Coinbase Pro was originally published in The Coinbase Blog on Medium, where people are continuing the conversation by highlighting and responding to this story.

Bitcoin expert Max Keiser has said that the Bank of England (BoE) will scramble to buy Bitcoin before the digital asset trades at $1 million.

His comments come after Bank of England’s deputy governor for financial stability, Jon Cunliffe, warned that cryptocurrencies could spark a global financial crisis unless tough regulations are introduced. Although regulators in many countries have started putting policies in place to manage the rapid growth of cryptocurrencies, Cunliffe said this must be pursued as a matter of urgency.

Bank of England Warns Against Crypto

The deputy Bank of England governor has called for strict regulations on Bitcoin and other cryptocurrencies. According to the Guardian, Cunliffe has played a central role in monitoring cryptocurrencies over recent years as an adviser to the G20’s financial stability board and the central banks’ overarching advisory body, the Geneva-based Bank of International Settlements.

Related Reading | Bank Of England Seeks To Strengthen Cryptocurrency Regulations

In a speech on Wednesday, October 13, Cunliffe compared the growth rate of the crypto market, from $16 billion five years ago to $2.3 trillion today, to the $1.2 trillion subprime mortgage market before the 2008 financial crash. He said there was a probability that financial markets could be rocked in a few years by an event of similar magnitude.

“When something in the financial system is growing very fast and growing in largely unregulated space, financial stability authorities have to sit up and take notice,” he said.

He also spoke about the majority of crypto-assets having no intrinsic value and could be worthless overnight. He stated emphatically how the crypto world is beginning to connect to the traditional financial system even though the space is still largely unregulated.

The banking chief added that there were “Financial stability risks currently are relatively limited, but they could grow very rapidly if, as I expect, this area continues to develop and expand at pace. How large those risks could grow will depend in no small part on the nature and on the speed of the response by regulatory and supervisory authorities.”

Related Reading | Bank of England Governor Still Isn’t a Fan of Bitcoin

His comments are similar to those of Bank of England Governor Andrew Bailey. In May, Bailey called crypto dangerous and warned that investors should be prepared to lose all their money due to the digital assets’ lack of intrinsic value.

Bitcoin Expert’s Response

Bitcoin expert Max Keiser responded to the Bank of England’s deputy governor’s recent warning about cryptocurrencies in a statement to Express.co.uk.

He said, “Bitcoin is designed to trigger a meltdown of the current fiat money banking system. This is a mathematically guaranteed outcome.”

BTC trading at over $60.8K | Source: BTCUSD on TradingView.com

Keiser implies that the BoE is grieving because Bitcoin killed central banks. “Bitcoin killed central banks. The Bank of England is in the second stage of the five stages of grief, the anger phase.”

He further pronounces that the Bank of England will eventually consider adopting Bitcoin.

“The bargaining phase will be their central bank digital currency stage and when that fails comes depression as the price tops £363,000 ($500,000) and then acceptance with the Bank of England scrambling to buy Bitcoin before it tops £727,000 ($1million) per coin,” Keiser says.

Featured image by Proactive investors, Chart from TradingView.com

Privacy is a complicated topic. Few would argue that privacy is not important. It’s generally more interesting to talk about things that are disputable. So, the limited arguments against privacy actually make it somewhat boring to discuss and easy to take for granted. As Edward Snowden famously said: “Arguing that you don’t care about privacy because you have nothing to hide is like arguing that you don’t care about free speech because you have nothing to say.”

However, what if your privacy is not a priority? What if your privacy is not guaranteed? What if everything you do is under constant surveillance?

You might fight back.

Unfortunately, this actually is the state of the cryptocurrency industry, and not enough people are in the fight to defend privacy.

Transparency vs. privacy

When I first read the Bitcoin (BTC) white paper in 2011, I fell in love with the vision for a peer-to-peer electronic cash system. Most societies have physical cash — legal tender — so, in a digital society, what is the physical cash equivalent? Satoshi Nakamoto seemed to come up with an elegant answer to that question, and a multi-trillion dollar market has emerged around it. Sadly, Satoshi’s original idea has fallen short in at least one area, and that’s privacy.

Legal tender is private. When someone exchanges coins or banknotes (aka “bills” in the U.S. and Canada) for a good or service, that transaction is only known to the two parties involved. Identification is requested if the good or service is restricted to certain age groups (beer runs aren’t for everyone). Further, if you hand a $10 bill to the lady at the local farmer’s market, she can’t look up how much you have left in your bank account.

However, transactions on the Bitcoin blockchain are radically transparent. This means transaction amounts, frequency and balances are all open for the entire public to see. The Bitcoin white paper only dedicates a half-page to the topic of privacy with suggested workarounds that don’t always work as intended, especially for second generation account-based blockchains such as Ethereum.

There are user guides on how to achieve more privacy using Bitcoin, but they are extremely complicated and generally recommend using tools that can be dangerous for users. There are also a few blockchain networks that have been designed with privacy as the default, but most do not support more complex programmability such as smart contracts, which enable new use cases involving business logic in decentralized finance (DeFi).

Related: DPN vs. VPN: The dawn of decentralized web privacy

Leaving privacy behind

Why has the blockchain community fallen short in making privacy a tier-one priority? For one, privacy has taken a back seat to three other priorities: security, decentralization and scalability. Nobody will argue that these three components aren’t important either. But do they have to be mutually exclusive to privacy?

Another reason privacy has not been prioritized is that it’s very hard to guarantee. Historically, privacy tools such as zero-knowledge proofs have been slow and inefficient, and making them more scalable is hard work. But, just because privacy is hard, does that mean it should not be a priority?

The last reason is probably the most concerning. There’s a myth in the media thatcrypto transactions are completely anonymous. They are not. This means that many people have been actively using crypto under the fallacy that their transactions are private. As blockchain network analysis tools become more sophisticated, the lack of anonymity increases. So, when does privacy become important enough to make it a priority?

Related: Bitcoin can’t be viewed as an untraceable ‘crime coin’ anymore

Privacy Finance

A friend of mine who has worked in the crypto industry full-time since 2015 recently asked me, “WTF is PriFi?”PriFi, or “Privacy Finance,” is the crypto industry’s admission that we royally screwed up with privacy. We screwed up so badly that, 12 years into this industry’s evolution, we are just now getting to the point where privacy is important enough to have its own hashtag.

So, where do we go from here to build more privacy that protects everyday crypto users and achieves the digital privacy equivalent of cash?

The first step ismore education. As society becomes increasingly digital, privacy is becoming harder to achieve. This starts with educating the media on the differences between secrecy and privacy. Secrecy is not wanting anyone to know something. Privacy is not wanting the whole world to know something. Secrecy is a privilege. Privacy is a right.

The next step isto make privacy simpler.Achieving privacy in crypto should not require clunky workarounds, shady tools or a deep expertise of complex cryptography. Blockchain networks, including smart contract platforms, should support optional privacy that works as easily as clicking a button.

The final step is to defend privacy. Privacy is a timely issue. The recent U.S. infrastructure bill includes a clause to extend section 6050I of the tax code, which requires individual counterparties to collect personal information on each other for cash transactions over $10,000, and applies it to cryptocurrencies. Coin Center, a pro-crypto nonprofit advocacy and research group, is preparing to challenge the constitutionality of this change for crypto. You can too, here.

Armed with proper education, an intuitive user experience, and motivation to make privacy a priority for crypto, we can defend our rights without being reckless and maintain sensible privacy on our own terms.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Warren Paul Anderson is vice president of product at Discreet Labs, which is developing Findora, a public blockchain with programmable privacy. Previously, Warren led product at Ripple for 4.5 years, working on the XRP Ledger, Interledger, & PayString protocols; the RippleX platform; and RippleNet’s On-Demand Liquidity enterprise product. Prior to Ripple, in 2014, Warren co-founded Hedgy, one of the first DeFi platforms for derivatives using programmable, escrowed smart contracts on the Bitcoin blockchain.

Payments processor Strike has announced the launch of a new feature that will allow users to convert their paychecks to bitcoin. This feature brings workers one step closer to collecting their paychecks in bitcoin. Instead of the employer paying out wages and salaries in BTC, employees can take the paychecks they receive and convert them to cryptocurrency in one easy step.

Receiving Paychecks In Bitcoin

Strike is enabling users to convert all or some of their paychecks into BTC. Instead of cashing into fiat and then having to change back to BTC, users can directly convert to BTC using the paycheck that they receive. The feature is known as “Pay Me in Bitcoin” was announced on Thursday and is one of Strike’s efforts to make BTC readily available to its users.

Related Reading | Why We Could See The First Approved U.S. Bitcoin ETF In October

Strike is best known for helping El Salvador in their journey to bitcoin adoption, but they are also a bitcoin-focused payments processor that allows users to receive and pay in BTC. And with the new feature, get paid in BTC with no hassles.

Strike completely bypasses the need for employers to adopt and start paying their employees in cryptocurrencies. Instead giving employees the power to decide if they would rather convert their paychecks to fiat currency or cryptocurrencies. This also means that employees are not limited by the payments options their employers use. It doesn’t matter the company individuals work for, they can choose to have their paychecks deposited in bitcoin.

BTC price trading above $61,300 | Source: BTCUSD on TradingView.com

Following The Lead Of Coinbase

Strike’s announcement of the “Pay Me in Bitcoin” feature comes only a few weeks after Coinbase launched a similar feature. In the announcement post, Coinbase shared that customers were now able to deposit their paychecks directly to cryptocurrencies to ease their trading activities and just like Strike, streamline the process of users converting their money to cryptocurrencies.

The feature has been welcome in the crypto space as investors can now decide to deposit their full paycheck or a portion of it into their cryptocurrency tradings accounts. Customers could also choose to deposit their paychecks directly to U.S. dollars on Coinbase, which they can then use to carry out their trading activities on the platform.

Related Reading | Bitcoin Breaks $60,000 Ahead Of SEC ETF Approvals

Similar to Coinbase, Strike announced that the feature will initially be available to users in the United States. Roll-outs for other countries may be in the works but there has been no confirmation of these. Although users can only convert their paycheck to bitcoin on Strike, Coinbase offers users a wider variety as they can convert their paychecks to the over 100 cryptocurrencies currently listed on the exchange.

Featured image from Inc. Magazine, chart from TradingView.com

The overall price action in the cryptocurrency market during 2021 has been an extension of the bull-run witnessed over the last months of 2020. Cardano (ADA) has since picked up a strong bullish momentum and managed to steal the show among the altcoins sphere, setting its tone as a real competitor among the majors.

Nowadays, according to Coinmarketcap, ADA exchanges hands at $2.22, with a market capitalization of around $72.90 billion, standing at fourth place in the ranking of the largest cryptos by market cap.

The project founded by Charles Hoskinson has also seen some improvements on the blockchain that bolstered the confidence among the virtual currency during the first months of the year. Most recently, in September, Cardano deployed its Alonzo hard fork.

Now, after cracking the $2.00 threshold and consolidating its yearly gains above that neighborhood, crypto traders are eyeing the next year’s forecasts. AI-based forecast models like WalletInvestors are putting ADA at $4.587 as of press time from a yearly perspective, while its five-year forecast says that Cardano’s coin could skyrocket towards $14.05

So, what would be the future of the price after the ongoing consolidation around $2.00 in 2022?

ADA Technical Analysis for 2022

As the year-end period looms and Bitcoin (BTC) is finally cracking above $60,000, which is the latest critical hurdle ahead of its all-time highs, ADA has been trapped in some sort of rangebound that hasn’t been resolved since the lows tested during September 21 at $1.90.

Suggested articles

Bloom Helps DeFi Go Beyond Collateralized Lending with OnRampGo to article >>

As a contraction has been developed across the board, the 200-period simple moving average (SMA) at the H4 chart is capping gains and limiting any further advance of ADA above $2.40.

ADA H4 Chart

That said, bulls need to crack above such an area in order to allow a golden crossover of the 50-period simple moving average with the 200 SMA and thus bolstering the bullish case. A golden crossover in the H4 chart is significant in the crypto markets, given that it’s a solid signal that could unleash a bullish force that can strengthen further. If that’s the case, ADA could prepare the ground for a bullish 2022 year that could take it to test levels around $5.00.

In fact, another forecast model, LongForecast, put the price of ADA at the Q4 2022 around $3.24, which is the average price that Cardano’s coin could aim in a possible bull-run.

Gene Simmons and ADA

But is this a too-optimistic view towards ADA? Ask Gene Simmons, rock legend and Kiss bassist who is a well-known ADA investor.

He claimed in February to had bought ADA coins and confirmed recently in an interview that he’s still holding them, suggesting that his investment has doubled since then. Moreover, Simmons said that he plans to keep holding his cryptos for at least ‘a decade.’

Cryptocurrency data aggregator CoinGecko has released its Q3 2021 report showing massive gains across several crypto market sectors.

Following the May market crash, Q3 began on a low ebb for the crypto space, with market capitalization even dipping further in late July below the $1.2 trillion, less than half of the $2.5 trillion all-time high recorded only two months prior.

However, market capitalization did recover in Q3, even rising as high as $2.3 trillion in early September.

According to the CoinGecko report, Bitcoin (BTC), gaming “coins,” and nonfungible tokens (NFTs) dominated the crypto market space in Q3.

Bitcoin recorded a 25% increase between Q2 and Q3 and has continued on this upward trajectory, even reaching $60,000 for the first time in five months.

The network’s hash rate also experienced a resurgence in Q3, indicating a recovery from China’s sweeping crackdown that forced miners to relocate overseas.

Gaming tokens like Axie Infinity (AXS), Illuvium (ILV), and Gala (GALA), as well as the NFT space in general, did record massive gains in Q3 as well.

AXS, in particular returned almost 1,000% quarter-on-quarter gains, with its 2021 performance topping 13,700%.

In terms of NFT trading volume, OpenSea continued its dominance of the market segment. Indeed, OpenSea and Rarible recorded a total trading volume of about $6.8 billion in Q3 according to the CoinGecko report.

Related: Crypto markets soar after Fed commits to printing and Evergrande plans to pay its debt

These significant market gains also came on the back of a storm of regulatory concerns regarding cryptocurrencies. Policymakers in the United States seemingly applied pressure with calls for stricter laws surrounding market segments like stablecoins.

Despite the steady gains recorded in Q3, the crypto market recovery is still some way off the activity levels seen before the May crash.

For one, CoinGecko reported that spot trading volume across the major centralized and decentralized exchanges declined over 42% in Q3.

Shiba Inu, one of the world’s most valuable cryptocurrency assets by market cap, has seen immense retail demand in the last few months. The meme coin started this year with a market cap of a few million dollars, now the digital asset has a market cap of approximately $10 billion.

SHIB (Coinmarketcap)

Dogecoin’s largest competitor developed a strong following in the last 8 months. While the biggest reason behind SHIB’s recent rally is its retail craze, institutional investors have started considering Shiba Inu as a good portfolio diversifier. Amid the latest price surge, large SHIB transactions have surged substantially, indicating that Shiba Inu whales are planning to hold the world’s 21st largest cryptocurrency for the next few years.

So, is it only FOMO (fear of missing out) or some serious investors have started adding Shiba Inu to their crypto portfolios? Finance Magnates asked crypto experts about their views on the latest SHIB rally and the importance of Shiba Inu as a portfolio diversifier.

Difficult to Ignore Shiba Inu

“6 months ago, if someone had asked me about “social awareness” tokens (meme coins) such as SHIB or DOGE, I would have NEVER considered them an investment. However, 6 months later, it is clear for me to see that you CANNOT ignore the social power of these tokens in terms of Return on Investment. So, there may be something to these tokens,” Johnny McCamley, Founder of CryptoClear, commented.

“The goal of SHIB was and still is to catch up to DOGE and ultimately surpass DOGE. It isn’t too far away at $10 Billion (SHIB), $30.8 Billion (DOGE). Again, this [is] illustrating that community is an extremely powerful catalyst- for tokens with close to zero utility,” he added.

Suggested articles

Bloom Helps DeFi Go Beyond Collateralized Lending with OnRampGo to article >>

While Shiba Inu is the biggest competitor of Dogecoin, its dynamics are completely different from other digital assets like XRP, BTC or ETH. McCamley believes that a meme coin portfolio is a risky option but an option at least.

“So, I have decided to create a ‘meme coin’ portfolio alongside my DeFi, Smart Contract portfolios. I have chosen to allocate $5K to this Meme tokens portfolio-spread amongst the top meme coins. To me, this is a complete ‘gamble’ riding on the social power of the community behind the token to drive the price, unlike actual utility for other Crypto Assets in my Portfolio. To me, this meme coin portfolio is the riskiest investment portfolio I have made EVER, but it is clear to see now, for me, that I should allocate a very small amount of capital to these projects, don’t sleep on meme coins,” McCamley said.

FOMO?

Joaquim Matinero Tor, a Blockchain Associate at Roca Junyent, said that he is not sure about the scalability ambitions of the Shiba Inu project, but FOMO is playing a major role in the latest price rally.

“Shiba Inu is still part of the FOMO strategy of most crypto adopters waiting for a new DogeCoin and obtain more than 7400% in less than 5 months. I’m quite sure SHIBA will jump also into an NFT ecosystem, but I’m not sure about its project and scalability ambitions. I could be wrong but nowadays only crypto-fans are interested in this kind of token,” Tor commented.

Starting today, BadgerDAO (BADGER) and Rarible (RARI) are available on Coinbase.com and in the Coinbase Android and iOS apps. Coinbase customers can now trade, send, receive, or store BADGER and RARI in most Coinbase-supported regions, with certain exceptions indicated in each asset page here. Trading for these assets is also supported on Coinbase Pro.

BADGER

BADGER is an Ethereum token that powers Badger DAO, a decentralized autonomous organization (DAO) focused on bringing Bitcoin into the decentralized finance (DeFi) ecosystem on Ethereum and other blockchains. BADGER is primarily used to govern the direction of Badger DAO and its products. BADGER can also be deposited into a Badger vault to boost yield for other deposits.

RARI RARI is an Ethereum token that powers Rarible, a community-owned marketplace for creating, selling, or collecting NFTs. RARI can be earned by using the platform and can be used to curate content and vote on platform upgrades.

One of the most common requests we hear from customers is to be able to buy and sell more cryptocurrencies on Coinbase. We announced a process for listing assets, designed in part to accelerate the addition of more cryptocurrencies. We are also investing in new tools to help people understand and explore cryptocurrencies. We launched informational asset pages (see BADGER and RARI), as well as a new section of the Coinbase website to answer common questions about crypto.

Customers can sign up for a Coinbase account here to buy, sell, convert, send, receive, or store e Coinbase Android and iOS apps. Coinbase customers can now trade, send, receive, or store BADGER and RARI today.

###

Please note: Coinbase Ventures may be an investor in the crypto projects mentioned here, and additionally, Coinbase may hold such tokens on its balance sheet for operational purposes. A list of Coinbase Ventures investments is available at https://ventures.coinbase.com/. Coinbase intends to maintain its investment in these entities for the foreseeable future and maintains internal policies that address the timing of permissible disposition of any related digital assets, if applicable. All assets, regardless of whether Coinbase Ventures holds an investor or Coinbase holds for operational purposes, are subject to the same strict review guidelines and review process.

This website contains links to third-party websites or other content for information purposes only (“Third-Party Sites”). The Third-Party Sites are not under the control of Coinbase, Inc., and its affiliates (“Coinbase”), and Coinbase is not responsible for the content of any Third-Party Site, including without limitation any link contained in a Third-Party Site, or any changes or updates to a Third-Party Site. Coinbase is not responsible for webcasting or any other form of transmission received from any Third-Party Site. Coinbase is providing these links to you only as a convenience, and the inclusion of any link does not imply endorsement, approval or recommendation by Coinbase of the site or any association with its operators.

Crypto is a new type of asset. Besides potential day to day or hour to hour volatility, each crypto asset has unique features. Make sure you research and understand individual assets before you transact.

All images provided herein are by Coinbase.

BadgerDAO (BADGER) and Rarible (RARI) are now available on Coinbase was originally published in The Coinbase Blog on Medium, where people are continuing the conversation by highlighting and responding to this story.

Today, we’re pleased to introduce our new regulatory framework, entitled Digital Asset Policy Proposal: Safeguarding America’s Financial Leadership (dApp). We hope this document will animate an open and constructive discussion regarding the role of digital assets in our shared economic future. Our goal is to thoughtfully and respectfully engage in the debate, and to offer good-faith suggestions for how the U.S. financial regulatory framework should adapt to two critical developments:

1. The blockchain-driven and decentralized evolution of the internet

2. The emergence of a distinctive asset class that is digitally native and empowers unique economic use cases

We understand that high-level proposals don’t become law overnight — nor should they. But what they can do is evolve the debate in ways that are helpful for everyone, including members of Congress who are increasingly focusing on this area.

A number of us have been working diligently on this for some time, consulting with experts, crypto builders, opinion leaders, and policymakers from across the country. We’ve also studiously read the commentary produced by our peers and others who are pushing the debate forward in thought-provoking and creative ways. This process of investigation and discovery has been remarkably eye-opening and invaluable to help us think deeply about the potential of these new and uniquely democratizing financial innovations.

Here are three consistent themes that surfaced from the past few weeks of intensive meetings:

A broad awareness is emerging on blockchain and distributed ledger technology’s potential; one that recognizes crypto could be an important catalyst of innovation, economic growth and financial inclusion in an increasingly digital world

The adoption rate of crypto is growing rapidly, and regulation has a vital role to play in protecting the consumer and providing certainty to market participants

American geopolitical strength and leadership is inextricably tied to the United States maintaining its technological leadership

We’d like to personally thank everyone we met with for their feedback, their candor, and their willingness to engage on some of the most profound and complex economic and societal questions we face. Let’s dive in.

The Market Context

Digital assets like Bitcoin, Ether, stablecoins, and other cryptocurrencies are now a mainstream part of the financial market ecosystem. In 2013, the market cap for the entire cryptocurrency market was around $1.5 billion. In 2021, that market cap has grown to $2 trillion. Adoption rates have seen a similarly astounding rate of growth with an estimated 1 million crypto users in 2013 to an estimated 330 million users worldwide today, with tens of millions in the United States alone.

But like the early days of the internet, the use cases for crypto are still in a nascent stage of development and adoption. However, what we’re seeing is societally powerful. Blockchain and distributed ledger technologies have accelerated the democratization of finance that began with the emergence of mobile payments. Whether factors such as lack of wealth, inaccessible infrastructure, or a range of societal factors have historically contributed to the 1.7 billion adults who remain unbanked today, the evolution of decentralized protocols and peer-to-peer marketplaces have the potential to resolve deep disparities and inequities.

Marketplaces for digital assets have emerged to offer a platform that facilitates the demand from Americans to access certain innovations in the way financial assets are transferred and traded. Retail and institutional traders have direct access to platforms that execute transactions 24 hours a day, seven days a week. Transactions settle in real time. A multitude of intermediaries is no longer needed as the digital asset market infrastructure has developed so that exchange and trading services, clearing, settlement, and custody can be provided effectively and more efficiently by the same entity.

We are seeing the beginning of more efficient, transparent, and cost-effective processes compared to those in traditional financial markets. These developments, in turn, will empower market participants with greater and more direct control over their trading decisions, increasing accessibility to financial services, reducing excess costs of the current system — costs too often borne by retail customers, and creating more transparency for regulators, who are already benefiting from new ways to engage in market surveillance and combat illicit finance.

Laws drafted in the 1930s to facilitate effective oversight of our financial system could not contemplate this technological revolution. Elements of those laws do not have room for the transformational potential that digital assets and crypto innovation make possible. They do not accommodate the efficiency, seamlessness, and transparency of digital asset markets, and thus risk serving as an unintended barrier to current innovations in the digital asset economy. For example, digital assets that are well established, broadly recognized, and fully decentralized, like Bitcoin and Ether, have technical characteristics that are well understood by the public. There is no information vacuum that immediately needs to be resolved. Not only are some of the financial rules of a paper-based system obsolete, but they are also an encumbrance to innovation, inclusion, and social welfare.

Forcing the full spectrum of digital assets into supervisory categories codified before the use of computers risks stifling the development of this transformational technology, thus pushing offshore the innovative center of gravity that currently sits in the United States. Doing this will have profoundly harmful economic implications and undermine the United States’ leadership at a time when technology is so critical to this country’s geopolitical strengths. We are seeing some legislatures at the state-level take important steps to give their residents access to these innovations, but there is still more work to be done.

Fostering this innovation is also critical because there are too many people in our society who do not see a place for themselves in our current financial system. According to the Federal Reserve, up to 22% of American households could be unbanked or underbanked. This could mean up to 55 million American adults don’t have access to key functions of our critical financial and societal architecture. Furthermore, even for those with a bank account and recognizing the dramatic advances in financial technologies, payments remain slow and cumbersome. Millions continue to pay too much and wait too long to transfer funds to loved ones overseas or to invest their money directly in projects and ideas they care about.

This exclusion of millions from the financial system is occurring as more and more Americans look for alternatives to traditional finance. Surveys show that a diverse group of Americans are availing of the unique and empowering financial opportunities that crypto affords. To help the public and the businesses that will provide the services for this new, thriving financial ecosystem, regulatory certainty for everyone is required.

Digital Asset Policy Proposal: Safeguarding America’s Financial Leadership (dApp)

Pillar One: Regulate Digital Assets Under a Separate Framework

As mentioned at the outset, the cryptoeconomy is defined by two concurrent innovations, both of which have manifold impacts on our financial system. The changes made possible by these two innovations are transformational, but do not easily fit within the existing financial system, which assumes that the structure of our financial markets will remain largely as they have been in the past. Our financial regulatory system is predicated on the ongoing existence of a series of separate financial market intermediaries — exchanges, transfer agents, clearing houses, custodians, and traditional brokers — because it never contemplated that distributed ledger and blockchain technology could exist. A new framework for how we regulate digital assets will ensure that innovation can occur in ways that are not hampered by the difficulty of transitioning from our legacy market structure.

Pillar Two: Designate One Regulator for Digital Asset Markets

To avoid fragmented and inconsistent regulatory oversight of these unique and concurrent innovations, responsibility over digital asset markets should be assigned to a single federal regulator. Its authority would include a new registration process established for entities that serve as marketplaces for digital assets (MDAs) and an appropriate disclosure regime to inform purchasers of digital assets. Platforms and services that do not custody or otherwise control the assets of a customer — including miners, stakers and developers — would need to be treated differently. Additionally, in the tradition of other markets, a dedicated self-regulatory organization (SRO) should be established to strengthen the oversight regime and provide more granular oversight of MDAs. Together, they should formulate new rules that permit the full range of digital asset services within a single entity: digital asset trading, transfer, custody, clearing, settlement, money payment, staking, borrowing and lending, and related incidental services. This two-tier regulatory structure will ensure efficient and streamlined regulation and oversight, and evolve elements of the existing frameworks to meet the requirements of our new technologically-driven financial system.

Pillar Three: Protect and Empower Holders of Digital Assets

This new framework should have three goals to ensure holders of digital assets are empowered and protected:

Enhance transparency through appropriate disclosure requirements,

Protect against fraud and market manipulation, and

Promote efficiency and strengthen market resiliency.

Each of these goals should be accomplished in recognition of the unique characteristics and risks of the underlying functionalities of digital assets.

Pillar Four: Promote Interoperability and Fair Competition

Innovation in decentralized protocol development and the peer-to-peer marketplace continues to produce novel approaches that allow greater financial access across all facets of society. To realize the full potential of digital assets, MDAs must be interoperable with products and services across the cryptoeconomy. If fully realized, this can enshrine fair competition, responsible innovation, and promote a thriving consumer and developer ecosystem.

What’s Next

We hope you take the time to evaluate our proposal. And if you do, consider sharing your thoughts. We’re also open-sourcing the framework through GitHub, so tell us what you think there, express your views directly to your elected officials, and be part of the conversation that will shape our shared financial future. We will also be convening a number of opportunities to hear from others who have made thoughtful contributions to the debate that we are hoping to advance today.

Thank you for reading.

Digital Asset Policy Proposal: Safeguarding America’s Financial Leadership was originally published in The Coinbase Blog on Medium, where people are continuing the conversation by highlighting and responding to this story.