Coinbase, a US-listed cryptocurrency exchange

Cryptocurrency Exchange

A cryptocurrency exchange is an online platform that supports the exchange of various currencies for a cryptocurrency or digital asset.Comparable to a generalized financial exchange, a crypto exchange’s core function is to permit and encourage the buying and selling of cryptos.This is accomplished by producing a stable trading environment suitable for traders nested through different locations around the world. Sometimes a crypto exchange may be referred to as a digital currency exchange (DCE) for short.How Does Trading Take Place on a Crypto Exchange?Cryptocurrency trading occurs over a centralized exchange, although these crypto exchanges should be used with caution given the implications that surround the custody of new assets. Similar to the banking industry, when a crypto exchange holds cryptocurrencies of users they accrue interest and are no longer classified as client money.These provide an accessible platform for not only companies, hedge funds, and retail traders for exchanging digital currencies.Additionally, crypto exchanges serve a critical role in producing stability within the cryptocurrency sector given how the sourcing and pricing of these assets are innately volatile. One could think of a crypto exchange as an intermediary who provides a service by connecting buyers and sellers from various markets under one roof. In exchange for facilitating trades and for services rendered, a digital currency exchange generally collects a fee of an outgoing transaction that averages between 0.20% to 0.25% or will request a deposit fee that has been known to be as high as 11% for credit card deposits. Crypto exchanges may also support the exchange of crypto tokens, such as the Binance Token, which is ranked as the 9th most valuable cryptocurrency in the world.

A cryptocurrency exchange is an online platform that supports the exchange of various currencies for a cryptocurrency or digital asset.Comparable to a generalized financial exchange, a crypto exchange’s core function is to permit and encourage the buying and selling of cryptos.This is accomplished by producing a stable trading environment suitable for traders nested through different locations around the world. Sometimes a crypto exchange may be referred to as a digital currency exchange (DCE) for short.How Does Trading Take Place on a Crypto Exchange?Cryptocurrency trading occurs over a centralized exchange, although these crypto exchanges should be used with caution given the implications that surround the custody of new assets. Similar to the banking industry, when a crypto exchange holds cryptocurrencies of users they accrue interest and are no longer classified as client money.These provide an accessible platform for not only companies, hedge funds, and retail traders for exchanging digital currencies.Additionally, crypto exchanges serve a critical role in producing stability within the cryptocurrency sector given how the sourcing and pricing of these assets are innately volatile. One could think of a crypto exchange as an intermediary who provides a service by connecting buyers and sellers from various markets under one roof. In exchange for facilitating trades and for services rendered, a digital currency exchange generally collects a fee of an outgoing transaction that averages between 0.20% to 0.25% or will request a deposit fee that has been known to be as high as 11% for credit card deposits. Crypto exchanges may also support the exchange of crypto tokens, such as the Binance Token, which is ranked as the 9th most valuable cryptocurrency in the world. Read this Term, has announced on Thursday that it added support for Solana on an initial phase. That said, users can now handle their Solana (SOL), and Solana tokens (SPL) alongside their tokens held on all of Wallet extension’s supported networks.

“Today’s update makes it easier to keep track of all your crypto across an ever-growing range of supported networks, without the need to manage multiple wallet apps. However, this launch is just the beginning — Coinbase Wallet plans to further integrate with the Solana ecosystem, including the ability for users to connect to Solana dapps, and the ability to view and manage their Solana NFTs directly within their Coinbase Wallet extension,” Coinbase noted in a statement published via its website.

Coinbase Wallet’s extension has support for other networks like Ethereum, Avalanche, Polygon, BNB Chain, among others. With the new support of Solana, the US-listed firm aims to unlock more of Web3 ‘without needing to manage multiple wallets.’

Solana Blockchain in Figures

It has been reported that over the past year, the blockchain

Blockchain

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others.

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others. Read this Term Solana has been growing the fastest, with a total locked value of over $7.35B and over 1,400 projects launched covering DeFi, NFTs, and Web3.

Until now, those interested in exploring the Solana ecosystem or holding SOL and SPL tokens had to create yet another crypto wallet, manage an additional app or browser extension, and keep track of their assets across multiple platforms. From now on, users of the Coinbase Wallet extension can store, send, and receive SOL and all of its SPL tokens.

“We want to empower millions of people to seamlessly participate in the exciting world of dapps and the larger crypto ecosystem. With its low fees and fast transaction times, Solana makes the world of crypto accessible to even more people and is a great introduction to web3,” Adam Zadikoff, Senior Product Manager at Coinbase, pointed out.

Coinbase, a US-listed cryptocurrency exchange

Cryptocurrency Exchange

A cryptocurrency exchange is an online platform that supports the exchange of various currencies for a cryptocurrency or digital asset.Comparable to a generalized financial exchange, a crypto exchange’s core function is to permit and encourage the buying and selling of cryptos.This is accomplished by producing a stable trading environment suitable for traders nested through different locations around the world. Sometimes a crypto exchange may be referred to as a digital currency exchange (DCE) for short.How Does Trading Take Place on a Crypto Exchange?Cryptocurrency trading occurs over a centralized exchange, although these crypto exchanges should be used with caution given the implications that surround the custody of new assets. Similar to the banking industry, when a crypto exchange holds cryptocurrencies of users they accrue interest and are no longer classified as client money.These provide an accessible platform for not only companies, hedge funds, and retail traders for exchanging digital currencies.Additionally, crypto exchanges serve a critical role in producing stability within the cryptocurrency sector given how the sourcing and pricing of these assets are innately volatile. One could think of a crypto exchange as an intermediary who provides a service by connecting buyers and sellers from various markets under one roof. In exchange for facilitating trades and for services rendered, a digital currency exchange generally collects a fee of an outgoing transaction that averages between 0.20% to 0.25% or will request a deposit fee that has been known to be as high as 11% for credit card deposits. Crypto exchanges may also support the exchange of crypto tokens, such as the Binance Token, which is ranked as the 9th most valuable cryptocurrency in the world.

A cryptocurrency exchange is an online platform that supports the exchange of various currencies for a cryptocurrency or digital asset.Comparable to a generalized financial exchange, a crypto exchange’s core function is to permit and encourage the buying and selling of cryptos.This is accomplished by producing a stable trading environment suitable for traders nested through different locations around the world. Sometimes a crypto exchange may be referred to as a digital currency exchange (DCE) for short.How Does Trading Take Place on a Crypto Exchange?Cryptocurrency trading occurs over a centralized exchange, although these crypto exchanges should be used with caution given the implications that surround the custody of new assets. Similar to the banking industry, when a crypto exchange holds cryptocurrencies of users they accrue interest and are no longer classified as client money.These provide an accessible platform for not only companies, hedge funds, and retail traders for exchanging digital currencies.Additionally, crypto exchanges serve a critical role in producing stability within the cryptocurrency sector given how the sourcing and pricing of these assets are innately volatile. One could think of a crypto exchange as an intermediary who provides a service by connecting buyers and sellers from various markets under one roof. In exchange for facilitating trades and for services rendered, a digital currency exchange generally collects a fee of an outgoing transaction that averages between 0.20% to 0.25% or will request a deposit fee that has been known to be as high as 11% for credit card deposits. Crypto exchanges may also support the exchange of crypto tokens, such as the Binance Token, which is ranked as the 9th most valuable cryptocurrency in the world. Read this Term, has announced on Thursday that it added support for Solana on an initial phase. That said, users can now handle their Solana (SOL), and Solana tokens (SPL) alongside their tokens held on all of Wallet extension’s supported networks.

“Today’s update makes it easier to keep track of all your crypto across an ever-growing range of supported networks, without the need to manage multiple wallet apps. However, this launch is just the beginning — Coinbase Wallet plans to further integrate with the Solana ecosystem, including the ability for users to connect to Solana dapps, and the ability to view and manage their Solana NFTs directly within their Coinbase Wallet extension,” Coinbase noted in a statement published via its website.

Coinbase Wallet’s extension has support for other networks like Ethereum, Avalanche, Polygon, BNB Chain, among others. With the new support of Solana, the US-listed firm aims to unlock more of Web3 ‘without needing to manage multiple wallets.’

Solana Blockchain in Figures

It has been reported that over the past year, the blockchain

Blockchain

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others.

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others. Read this Term Solana has been growing the fastest, with a total locked value of over $7.35B and over 1,400 projects launched covering DeFi, NFTs, and Web3.

Until now, those interested in exploring the Solana ecosystem or holding SOL and SPL tokens had to create yet another crypto wallet, manage an additional app or browser extension, and keep track of their assets across multiple platforms. From now on, users of the Coinbase Wallet extension can store, send, and receive SOL and all of its SPL tokens.

“We want to empower millions of people to seamlessly participate in the exciting world of dapps and the larger crypto ecosystem. With its low fees and fast transaction times, Solana makes the world of crypto accessible to even more people and is a great introduction to web3,” Adam Zadikoff, Senior Product Manager at Coinbase, pointed out.

Coinbase Wallet browser extension now offers support for sending, receiving, and storing Solana and SPL tokens

By Adam Zadikoff, Senior Product Manager

Making web3 more user-friendly means more ways to interact and connect with dapps across a wide range of blockchains and networks. Today, we’re introducing our initial phase of support for Solana. Users can now manage their Solana (SOL) and Solana tokens (SPL) alongside their tokens held on all of Coinbase Wallet extension’s supported networks, including Ethereum, Avalanche, Polygon, BNB Chain, and many more. This allows users to unlock more of web3 without needing to manage multiple wallets.

Over the past year, there has been an explosion of interest in web3 and decentralized applications, including NFTs and decentralized finance (DeFi). One of the blockchain networks that has seen a surge in usage is Solana, which has built a vibrant community of both developers and users along the way.

Today’s update makes it easier to keep track of all your crypto across an ever-growing range of supported networks, without the need to manage multiple wallet apps. However, this launch is just the beginning — Coinbase Wallet plans to further integrate with the Solana ecosystem, including the ability for users to connect to Solana dapps, and the ability to view and manage their Solana NFTs directly within their Coinbase Wallet extension.

Over the past year, there has been a surge in interest and usage of blockchain networks. While this has resulted in exciting new projects, ecosystems, and communities, it has also revealed scaling issues that have the potential to leave users with high network fees (or “gas”) and long transaction processing times.

Many users have been looking for networks that are optimized for scale, offering low-cost transactions and fast transaction times. One of the fastest-growing blockchains over the past year has been Solana, which now has over $7.35B in total locked value (TLV) and more than 1,400 projects launched, spanning DeFi, NFTs, and web3. It is home to a number of well-known NFT projects including the Degenerate Apes collection, and DeFi protocols including the decentralized exchange, Serum.

Up until now, users who wanted to explore the Solana ecosystem or hold SOL and SPL tokens had to create yet another crypto wallet, manage an additional app or browser extension, and keep track of their assets across multiple surfaces. Starting today, Coinbase Wallet extension users can store, send, and receive Solana (SOL) and all of its SPL tokens alongside all of their EVM-compatible assets, including tokens held on Ethereum, Avalanche, Polygon, BNB Chain, and many more.

If you already have a Solana wallet, such as Phantom or Solflare, it’s quick and easy to import your existing Solana self-custody wallet into Coinbase Wallet. All you’ll need is the latest Coinbase Wallet desktop extension and your Solana wallet’s recovery phrase. You can read our step-by-step instructions on the Wallet extension guide for more information.

If you don’t already have a Solana wallet, the Coinbase Wallet extension will automatically create one for you. And with recently launched Coinbase Pay, it’s easier than ever to add SOL to your Coinbase Wallet extension — you can safely and securely transfer SOL you already hold in your Coinbase account to your Coinbase Wallet, or buy SOL using your stored payment methods.

Today’s release makes SOL and SPL tokens available on the browser extension. This means that if you use Coinbase Wallet on both mobile and desktop, you’ll only see the SOL and SPL tokens that are in your wallet when using Coinbase Wallet extension. You will not be able to see them in the Coinbase Wallet mobile app, however your tokens are safely stored in your wallet.

How to import an existing Solana-based wallet into Coinbase Wallet

We want to empower millions of people to seamlessly participate in the exciting world of dapps and the larger crypto ecosystem. With its low fees and fast transaction times, Solana makes the world of crypto accessible to even more people and is a great introduction to web3.

Today’s launch is just the beginning of Coinbase Wallet and the Solana ecosystem coming together. In the coming months, we’ll be adding support for Solana NFTs and the ability for you to connect your wallet to Solana dapps to interact with everything the Solana ecosystem has to offer.

You can experience the latest enhancements for yourself by downloading Coinbase Wallet’s browser extension for free from the Chrome Web Store. Make sure to follow us on Twitter @CoinbaseWallet for the latest Wallet-related news and product announcements.

—

Information is provided for informational purposes only and is not investment advice. This is not a recommendation to buy or sell a particular digital asset. Coinbase Wallet is a self-custody wallet providing software services subject to Coinbase Wallet Terms of Service and Privacy Policy. Coinbase Wallet is distinct from Coinbase.com, and private keys for Coinbase Wallet are stored directly by the user and not by Coinbase. Fees may apply. You do not need a Coinbase.com account to use Coinbase Wallet.

Singapore, 14th March 2022 — Decentralized cross-chain lending platform Fountain Protocol has launched a liquidity mining program on the Oasis mainnet, attracting over $15 million in TVL (total value locked) within 24 hours.

The strong launch earns Fountain Protocol a third-place ranking as compared to all other protocols on the…

Examining crypto’s usage in Ukraine, sanctions, and the Biden Executive Order

Around the Block from Coinbase Ventures sheds light on key trends in crypto. Written by Connor Dempsey

There’s a gravitational shift taking place within our industry. Since Russia’s shocking invasion of Ukraine, crypto has been:

used to crowdfund tens of millions for the Ukrainian defense

incorrectly speculated as a viable avenue for the Russian government to evade sanctions

the focus of a historic Executive Order put forward by the Biden administration

At this point, one thing is clear: this technology is a major emerging force in the geopolitical landscape. In this edition of Around The Block, we examine crypto in a geopolitical context, along with the difficult questions the world is asking.

An email address for money

In the aftermath of Russia’s attack on Ukraine, crypto’s power for coordinating economic activity was put on full display once the official Ukrainian twitter account tweeted out a plea for aid, accompanied with two long strings of letters and digits.

These long strings of characters were the Bitcoin and Ethereum addresses of the Ukrainian government, and the tweet represents the first time a nation state has ever sought aid directly in crypto. At a time when the Ukrainian government and banking sites were being flooded with DDoS (denial of service) attacks, and crowdfunding platforms were deplatforming organizations raising aid for Ukraine, the utility of permissionless, borderless networks for sending money was vividly illustrated.

At this time of writing, the Ukrainian government has collected over $50M in Bitcoin, ETH, ERC-20 stablecoins, and in other assets like DOT, DAI, and even Dogecoin.

The Ukrainian government has said that it has been using the funds to buy military supplies including bullet-proof vests, drones, gasoline, and night vision goggles. What’s more interesting is that 40% of suppliers have accepted payment in crypto.

Many have pointed out the oddity of private citizens from around the world essentially crowdfunding a war effort. Yet another sign of just how unprecedented all of this is.

NFTs enter the fold

Fungible crypto assets weren’t the only donations to pour into the Ukrainian government’s crypto wallet. NFT enthusiasts also answered the call, donating over 200 pieces of digital art work and even ENS addresses. Most notably, a rare CryptoPunk worth an estimated $200,000 was donated.

What’s interesting is that since the ownership provenance of the CryptoPunk will forever be associated with the defense of Ukraine, this added historical significance could raise its value over the long term.

The NFT aid didn’t stop there, as they were also combined with another crypto primitive to support the defense of Ukraine: DAOs.

UkraineDAO

Decentralized autonomous organizations were cast into the limelight last year after ConstitutionDAO crowdsourced $40M in under a week in a bid to buy one of the original copies of the US Constitution. While the bid ultimately failed, it underscored the power that these software enabled organizations have for coordinating economic activity at the speed of the internet.

After a Ukrainian NGO (non-government organization) supporting the war effort called Come Back Alive was de-platformed from crowdfunding platform Patreon for supporting military activity, they also turned to crypto. Shortly thereafter, UkraineDAO was created to help support this NGO.

The DAO minted a 1:1 NFT of the Ukrainian flag and put it up on PartyBid, which allows groups to pool funds to buy NFTs. In essence, the DAO created its own NFT, crowdsourced as much money as they could to buy it from themselves and then donated the proceeds to Come Back Alive. All told, they raised $6.7M. They also distributed commemorative “valueless” tokens called LOVE to those who donated.

Crypto on the main stage

Between the Ukrainian government and various NGOs, over $80M and counting in aid has been raised. While in the grand scheme of things this amount is a nominal sum not likely to turn the tides of war, it’s also far from insignificant. The sum represents over 20% of the $350M pledged by the Biden administration and is a powerful display of the promise that decentralized, borderless money holds.

Slowmist, where we’re pulling this data, also noted that when you factor in other organizations and cryptocurrencies they’re not tracking, the full figure is likely over $100M. The Giving Block, for example, raised over $2.3M in crypto donations for over 20 non-profits supporting Ukrainian relief.

Beyond support of the Ukrainian government and organizations, crypto has also proven useful for individual Ukrainians affected by the crisis. One Ukrainian who fled to Kazakhstan reported that he lost access to his savings and that his credit cards were no longer functioning, leaving crypto as his only financial life raft: yet another example of the utility of permissionless finance.

At their core, Bitcoin, Ethereum, and the like are neutral technologies that anyone with an internet connection can use. While we celebrate the use of these neutral technologies to help a nation defend itself against a foreign invader and as a lifeline for refugees, it also begs the question: what about their use by those on the other side of the conflict? Principally, the Russian government.

The burning question

Western governments responded to Russian aggression with unprecedented sanctions against the Russian government. This coincided with widespread narratives surrounding the potential for cryptocurrencies to be used to circumvent those very sanctions.

Before we examine the fact or fiction behind these claims, it helps to understand what these sanctions entail.

Russian sanctions

Since Russia invaded Ukraine, governments around the world, including the U.S., have imposed sanctions targeting the Central Bank of Russia, major Russian commercial banks and companies, Vladimir Putin, Russian elites, among others. In aggregate, these sanctions cut targeted individuals and entities off from international banking and in many instances, freezes their assets.

Among the most substantial sanctions imposed was kicking major Russian banks out of SWIFT, which is the financial network used by over 11,000 banks and institutions to move trillions of dollars across borders. This severely limits Russia’s ability to receive payments for oil and gas: their main export. For context, when Iranian banks were banned from SWIFT in 2012, and sanctions were imposed on Iranian oil purchasers, Iran lost nearly half of its oil export revenue and 30% of its foreign trade.

The most drastic sanction is from the US, UK, and EU banning transactions with the Russian Central Bank. The Russian Central Bank holds roughly $630B in the form of the world’s major reserve currencies — the dollar, euro, pound, yuan — as well as 2,300 tons of gold. With this sanction, Russia suddenly has no one to sell its reserves to, rendering its entire stockpile useless.

Is crypto their answer?

We’ve seen public speculation on how crypto could be used to evade those sanctions. However, that speculation has been unfounded as the crypto market is simply not large enough to help Russia meaningfully circumvent them.

Consider the Russian Central Bank’s $630B in immobilized assets. That’s 80% of Bitcoin’s market cap and larger than the rest of the crypto market put together. Converting that much fiat into crypto would take 5–10x the total daily traded volume of all digital assets, so the liquidity just isn’t there.

Additionally, as our Chief Legal Officer previously pointed out, trying to obscure large transactions using open and transparent crypto technology would be far more difficult than other established methods (e.g., using fiat, art, gold, or other assets).

The Biden Executive Order

As crypto played a significant role in the defense of Ukraine, it was also cast into the fore of the American political system. Late last week, the Biden Administration published its long awaited Executive Order on digital asset regulation.

The Executive Order simply directed federal agencies to study the benefits and risks of digital assets, as opposed to putting any immediate legislation into action. On one hand, many were pleasantly surprised with the optimistic tone of the EO, as it acknowledged crypto and Web3 technologies as critical for the future of U.S. national economic competitiveness. On the other, the report focused more on the potential risks of crypto rather than its societal benefits.

The EO calls on a total of 23 federal government agencies, organizations, and White House Offices to assemble huge reports on the risks stemming from crypto. This outsized focus on risk, when compared to past EOs, has caused some people to worry that the Biden Administration doesn’t fully recognize the power and potential of digital assets, even as that power is being plainly demonstrated on the world stage.

While the EO may have felt like a milestone, it is ultimately the start of a long road ahead. One in which the whole of the US government will finally seek to fully understand the importance of this technology. It is critical that the government fully explores not only the risks, but also the benefits that digital assets bring, with enough transparency to allow the public to weigh-in on a federal approach to regulation.

Ultimately, this presents a tremendous opportunity for the industry to engage with regulators about how to best embrace the transformational nature of crypto and Web3 technologies.

Closing thought

To sum it all up, regardless of how you feel about crypto’s application in funding a war effort or the increased attention it’s receiving from the most powerful government in the world, it’s apparent that we’ve entered uncharted territory: this next phase of crypto adoption will look drastically different from the last.

ATB Podcast: Crypto’s Role in the Ukraine Crisis with Elliptic’s Dr. Tom Robinson

This year, Silvergate Capital paid $182 million for Diem’s technology assets, bringing an end to Facebook’s plan to build a crypto payments network.

The deal underscores how the social network giant, now Meta, has just a limited number of regulatory-approved options for becoming a prominent player in the blockchain space.

These well-known investors participated in a strategic investing round, which was led by investors including Tiger Global, Multicoin Capital, Katie Haun and Coinbase Ventures.

Blockchain System For Aptos

Aptos, a project founded by ex-Facebook employees who just left the firm in December, has already received unicorn money from Andreessen Horowitz and other prominent web3 investors.

Aptos Chief Executive Officer Mo Shaikh said in a recent blog post:

“We are the founders, researchers, designers, and builders of Diem, the first blockchain developed for this purpose… while the rest of the world never saw what we produced, our job is far from done.”

Aptos has disclosed that it has raised $200 million in capital from Tiger Global, Katie Haun, Multicoin Capital, 3 Arrows Capital, FTX Ventures, and Coinbase Ventures to pursue its goal of establishing a blockchain scalability system.

Another prominent first-round investor is Silvergate Capital, while the Aptos team assures that they will not license or use any of Silvergate’s Diem IP as they develop their blockchain.

Related Article | Gloomy Crypto Future? Book Author Warns We’re In The Biggest Bubble In History

Crypto total market cap at $1.78 trillion on the daily chart | Source: TradingView.com

No Direct Link With Facebook

However, some in the crypto industry are skeptical of implementing Facebook’s web3 vision, even though Diem proponents like Andreessen Horowitz may rally behind a group aiming to take up the effort.

“To be clear, we have no official connection with Facebook and no funding from them,” Shaikh said.

As a result, Aptos sees another challenge in recruiting developers. Move, an open-source programming language developed by Meta, is being used to lure new developers to the company.

The Aptos Devnet

Instead of building on top of existing decentralized networks like Ethereum or Solana, Aptos will create its own decentralized network from the ground up.

Additionally, Aptos launched its “devnet,” which will allow developers to explore and build on the Aptos blockchain before its public release, which the company expects to take place in the third quarter this year.

The fundamental objective of Aptos is to develop a blockchain that is more scalable, faster, and has cheaper transaction fees than the current major networks.

Customers that are interested in embracing blockchain technology should expect a more stable and dependable network from the project’s developers.

Related Article | Abra CEO Predicts Ethereum Could Reach $40,000 – But Some Fintech Analysts Don’t Agree

Featured image from SiliconANGLE, chart from TradingView.com

In a bipartisan letter put forward by Republican Minnesota Congressman Tom Emmer, a cohort of Congress members has written to Securities and Exchange Commission (SEC) Chairman Gary Gensler, challenging the regulator’s scrutiny of cryptocurrency firms and expressing concern that “overburdensome” investigation may be suffocating the crypto industry.

They suggest the SEC is drowning companies in paperwork in contravention of the SEC’s stated aims and mandated jurisdiction.

Emmer tweeted to his 51,000 followers:

“My office has received numerous tips from crypto and blockchain firms that SEC Chair @GaryGensler’s information reporting ‘requests’ to the crypto community are overburdensome, don’t feel particularly… voluntary… and are stifling innovation.”

In the letter, which was co-signed by four Democrats and three Republicans, all of whom are members of the bipartisan Congressional Blockchain Caucus, Emmer asserts that the Gary Gensler-led SEC is abusing its investigative powers and overburdening crypto firms — claiming that the regulator has been using the Division of Enforcement and Division of Examination authorities to unfairly bog down crypto and blockchain companies in excessive paperwork.

The legislators believe the regulator has been misusing these divisions and pointed out limitations in the SEC’s mandated jurisdiction,

“It appears there has been a recent trend towards employing the Enforcement Division’s investigative functions to gather information from unregulated cryptocurrency and blockchain industry participants in a manner inconsistent with the Commission’s standards for initiating investigations.”

The Congress members believe the SEC could be violating the Paperwork Reduction Act (PRA) of 1980, which regulates the volume of paperwork that any individual or private entity needs to provide to a federal agency.

Managing Partner at emerging technologies legal firm Brookwood, Collins Belton lauded Emmer’s work on Twitter, saying that the requests in the letter “will not paint the commission in a good light.”

This is actually an interesting move I wasn’t expecting, clearly some of y’all in DC have gone to work. The requests in the letter are particularly on point and will *not* paint the commission in a good light imo, and that’s solely off of the requests I’m personally aware of. https://t.co/ElguJ77sEa

Belton also shared that he was “really glad” the issues raised by Emmer and the other Congress members were coming to light, as legal privilege had made it difficult for him to express concerns about the SEC publicly.

“I haven’t been able to discuss much in public as much as I would like to due to privilege issues, but with answers to some of these, I think the public will see just how absurdly broad some of these requests have been.”

Related: Motions denied for both SEC and Ripple as battle continues

Emmer has been a staunch defender of blockchain technology and cryptocurrency in the past, introducing the Security Clarity Act in Jul. 2021, which aimed to provide a clear legal definition for digital assets. Emmer hopes that the bill will allow blockchain entrepreneurs to distribute their assets without fear of any additional regulatory burdens, after meeting the requirements set out in the bill. The bill is still in its introduction phase and is yet to pass through the House of Representatives.

By Prakash Hariramani, Senior Director, Product Management, and Bipul Sinha, Senior Product Manager

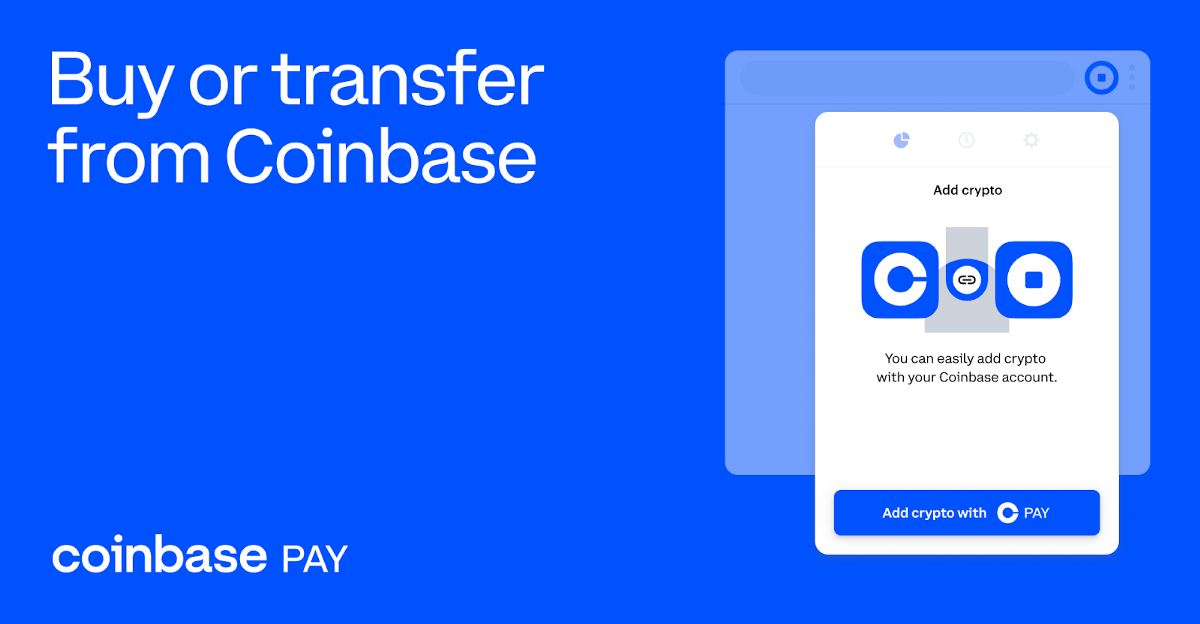

Today, we are introducing Coinbase Pay, the easiest way for Coinbase users to fund their Coinbase Wallet from the Chrome browser extension and explore web3.

Over the past year, DeFi, NFTs, and other web3 services have seen tremendous adoption. However, a key step in being able to access and use these services — funding a self-custody wallet — is a cumbersome process that involves multiple steps, switching between apps, and manual transfers.

Coinbase Pay eliminates these steps, and makes it easy and intuitive for anyone to participate in DeFi or purchase NFTs, in just a few clicks.

Cash. Click. Crypto.

Before Coinbase Pay, users who wanted to add funds to their Coinbase Wallet from the browser extension needed to navigate to Coinbase.com, sign in to their account, copy-paste their wallet address, and manually transfer funds from their Coinbase account.

The process was not only cumbersome, but also left the user vulnerable to user error. For example, if funds were accidentally sent to the wrong wallet address, they would be irretrievable.

Coinbase Pay makes the process faster, easier, and more secure than ever before. All you need to do is select “Add crypto with Coinbase Pay” when you want to add crypto to your Coinbase Wallet extension.

Next, you simply select the currency you want to add to your wallet, specify the amount, confirm the transaction–and that’s it. No more switching between apps, copy-pasting addresses, and manually transferring funds.

Coinbase users based in the US and Canada can currently use their debit cards and bank accounts for transfers, with more payment options enabled globally soon.

First-time users of Coinbase Wallet will need to link their self-custody wallet to their Coinbase account before being able to use Coinbase Pay.

Making it even easier to access the world of DeFi, NFTs, and more

At Coinbase, our mission is to increase economic freedom in the world. A key part of realizing this mission is building crypto products and services that are easy-to-use and accessible. Coinbase Pay makes it even easier for users to get web3-ready with Coinbase Wallet.

With the Coinbase Wallet extension, your Chrome browser can securely interact and engage with all manner of web3 applications. Kickstart your NFT collection, earn yield through DeFi lending protocols, and grow your crypto portfolio with hundreds of thousands of tokens supported via decentralized exchanges (DEXes).

And now you can engage with dapps with greater peace of mind, knowing that your payment credentials remain safely stored within Coinbase.

Looking forward

We are continuing to build new features into Coinbase Wallet to make it the most user-friendly and accessible self-custody wallet in the world, making it easier for more users to enter the world of web3. We will also continue to expand Coinbase Pay to bring the benefits of seamless fiat onramp to the crypto ecosystem. Stay tuned for more updates.

Make sure to follow us on Twitter for the latest news about Coinbase Wallet and Coinbase Pay.

Coinbase Wallet is a self-custody wallet providing software services subject to Coinbase Wallet Terms of Service and Privacy Policy. Coinbase Wallet is distinct from Coinbase.com, and private keys for Coinbase Wallet are stored directly by the user and not by Coinbase. Fees may apply. You do not need a Coinbase.com account to use Coinbase Wallet.

ConsenSys, a blockchain

Blockchain

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others.

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others. Read this Term technology solutions provider, announced on Tuesday that it had closed a $450 million financing round, bringing its valuation to over $7 billion. According to the press release, ParaFi Capital led the funding raise.

New investors joined them, including Temasek, SoftBank Vision Fund 2, Microsoft, Anthos Capital, Sound Ventures, and C Ventures. The United Talent Agency’s venture fund, UTA VC, and Third Point also participated in this round of funding. In this transaction, Sullivan & Cromwell LLP acted as ConsenSys’ legal advisor.

“I think of ConsenSys as a broad and deep capabilities machine for the decentralized protocols ecosystem, able to rapidly capitalize at scale on fundamental new constructs that emerge, such as developer tooling, tokenization, token launches, wallets, security audits, DeFi (1.0, 2.0 and beyond), NFTs, bridges, Layer-2 scaling, DAOs, and more. This view has resonated with our crypto native and growth investors in a Series D that will enable us to execute powerful growth strategies,” Joseph Lubin, Founder and CEO of ConsenSys, commented.

According to ConsenSys’ treasury strategy, the proceeds from this round will be converted to ETH in order to rebalance the ratio of ETH to USD equivalents. They added to ConsenSys’ “ultra sound money” position in advance of Ethereum’s merger to Proof of Stake.

A significant amount of Ethereum, stablecoins, and other crypto assets have been accumulated by ConsenSys over the years, which is actively investing them in DeFi protocols and via staking

Staking

Staking is defined as the process of holding funds in a cryptocurrency wallet to support the operations of a blockchain network. In particular, staking represents a bid to secure a volume of crypto to receive rewards. In most case however, this process relies on users participating in blockchain-related activities via a personal crypto wallet.The concept of staking is also closely tied to the Proof-of-Stake (PoS). PoS is a type of consensus algorithm in which a blockchain network aims to achieve distributed consensus.This notably differs from Proof-of-Work (PoW) blockchains that instead rely on mining to verify and validate new blocks.Conversely, PoS chains produce and validate new blocks through staking. This allows for blocks to be produced without relying on mining hardware. As such, instead of competing for the next block with heavy computation work, PoS validators are selected based on the number of coins they are committing to stake.Users that stake larger amounts of coins have a higher chance of being chosen as the next block validator. Staking ExplainedStaking requires a direct investment in the cryptocurrency, while each PoS blockchain has its particular staking currency.The production of blocks via staking enables a higher degree of scalability. Moreover, some chains have also moved to adopt the Delegated Proof of Staking (DPoS) model. DPoS allows users to simply signal their support through other participants of the network. In other words, a trusted participant works on behalf of users during decision-making events.The delegated validators or nodes are the ones that handle the major operations and overall governance of a blockchain network. These participate in the processes of reaching consensus and defining key governance parameters.

Staking is defined as the process of holding funds in a cryptocurrency wallet to support the operations of a blockchain network. In particular, staking represents a bid to secure a volume of crypto to receive rewards. In most case however, this process relies on users participating in blockchain-related activities via a personal crypto wallet.The concept of staking is also closely tied to the Proof-of-Stake (PoS). PoS is a type of consensus algorithm in which a blockchain network aims to achieve distributed consensus.This notably differs from Proof-of-Work (PoW) blockchains that instead rely on mining to verify and validate new blocks.Conversely, PoS chains produce and validate new blocks through staking. This allows for blocks to be produced without relying on mining hardware. As such, instead of competing for the next block with heavy computation work, PoS validators are selected based on the number of coins they are committing to stake.Users that stake larger amounts of coins have a higher chance of being chosen as the next block validator. Staking ExplainedStaking requires a direct investment in the cryptocurrency, while each PoS blockchain has its particular staking currency.The production of blocks via staking enables a higher degree of scalability. Moreover, some chains have also moved to adopt the Delegated Proof of Staking (DPoS) model. DPoS allows users to simply signal their support through other participants of the network. In other words, a trusted participant works on behalf of users during decision-making events.The delegated validators or nodes are the ones that handle the major operations and overall governance of a blockchain network. These participate in the processes of reaching consensus and defining key governance parameters. Read this Term using its own financial infrastructures, such as MetaMask Institutional and Codefi Staking.

MyCrypto Acquisition

Recently, ConsenSys announced the acquisition of MyCrypto, a market-leading Web3 wallet. Following the acquisition, ConsenSys will combine MyCrypto with its popular MetaMask wallet.

MetaMask and MyCrypto will integrate their efforts under a shared brand to enhance the security of all their products and build a cohesive user experience across browser, extension, mobile and desktop wallets.

ConsenSys, a blockchain

Blockchain

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others.

Blockchain comprises a digital network of blocks with a comprehensive ledger of transactions made in a cryptocurrency such as Bitcoin or other altcoins.One of the signature features of blockchain is that it is maintained across more than one computer. The ledger can be public or private (permissioned.) In this sense, blockchain is immune to the manipulation of data making it not only open but verifiable. Because a blockchain is stored across a network of computers, it is very difficult to tamper with. The Evolution of BlockchainBlockchain was originally invented by an individual or group of people under the name of Satoshi Nakamoto in 2008. The purpose of blockchain was originally to serve as the public transaction ledger of Bitcoin, the world’s first cryptocurrency.In particular, bundles of transaction data, called “blocks”, are added to the ledger in a chronological fashion, forming a “chain.” These blocks include things like date, time, dollar amount, and (in some cases) the public addresses of the sender and the receiver.The computers responsible for upholding a blockchain network are called “nodes.” These nodes carry out the duties necessary to confirm the transactions and add them to the ledger. In exchange for their work, the nodes receive rewards in the form of crypto tokens.By storing data via a peer-to-peer network (P2P), blockchain controls for a wide range of risks that are traditionally inherent with data being held centrally.Of note, P2P blockchain networks lack centralized points of vulnerability. Consequently, hackers cannot exploit these networks via normalized means nor does the network possess a central failure point.In order to hack or alter a blockchain’s ledger, more than half of the nodes must be compromised. Looking ahead, blockchain technology is an area of extensive research across multiple industries, including financial services and payments, among others. Read this Term technology solutions provider, announced on Tuesday that it had closed a $450 million financing round, bringing its valuation to over $7 billion. According to the press release, ParaFi Capital led the funding raise.

New investors joined them, including Temasek, SoftBank Vision Fund 2, Microsoft, Anthos Capital, Sound Ventures, and C Ventures. The United Talent Agency’s venture fund, UTA VC, and Third Point also participated in this round of funding. In this transaction, Sullivan & Cromwell LLP acted as ConsenSys’ legal advisor.

“I think of ConsenSys as a broad and deep capabilities machine for the decentralized protocols ecosystem, able to rapidly capitalize at scale on fundamental new constructs that emerge, such as developer tooling, tokenization, token launches, wallets, security audits, DeFi (1.0, 2.0 and beyond), NFTs, bridges, Layer-2 scaling, DAOs, and more. This view has resonated with our crypto native and growth investors in a Series D that will enable us to execute powerful growth strategies,” Joseph Lubin, Founder and CEO of ConsenSys, commented.

According to ConsenSys’ treasury strategy, the proceeds from this round will be converted to ETH in order to rebalance the ratio of ETH to USD equivalents. They added to ConsenSys’ “ultra sound money” position in advance of Ethereum’s merger to Proof of Stake.

A significant amount of Ethereum, stablecoins, and other crypto assets have been accumulated by ConsenSys over the years, which is actively investing them in DeFi protocols and via staking

Staking

Staking is defined as the process of holding funds in a cryptocurrency wallet to support the operations of a blockchain network. In particular, staking represents a bid to secure a volume of crypto to receive rewards. In most case however, this process relies on users participating in blockchain-related activities via a personal crypto wallet.The concept of staking is also closely tied to the Proof-of-Stake (PoS). PoS is a type of consensus algorithm in which a blockchain network aims to achieve distributed consensus.This notably differs from Proof-of-Work (PoW) blockchains that instead rely on mining to verify and validate new blocks.Conversely, PoS chains produce and validate new blocks through staking. This allows for blocks to be produced without relying on mining hardware. As such, instead of competing for the next block with heavy computation work, PoS validators are selected based on the number of coins they are committing to stake.Users that stake larger amounts of coins have a higher chance of being chosen as the next block validator. Staking ExplainedStaking requires a direct investment in the cryptocurrency, while each PoS blockchain has its particular staking currency.The production of blocks via staking enables a higher degree of scalability. Moreover, some chains have also moved to adopt the Delegated Proof of Staking (DPoS) model. DPoS allows users to simply signal their support through other participants of the network. In other words, a trusted participant works on behalf of users during decision-making events.The delegated validators or nodes are the ones that handle the major operations and overall governance of a blockchain network. These participate in the processes of reaching consensus and defining key governance parameters.

Staking is defined as the process of holding funds in a cryptocurrency wallet to support the operations of a blockchain network. In particular, staking represents a bid to secure a volume of crypto to receive rewards. In most case however, this process relies on users participating in blockchain-related activities via a personal crypto wallet.The concept of staking is also closely tied to the Proof-of-Stake (PoS). PoS is a type of consensus algorithm in which a blockchain network aims to achieve distributed consensus.This notably differs from Proof-of-Work (PoW) blockchains that instead rely on mining to verify and validate new blocks.Conversely, PoS chains produce and validate new blocks through staking. This allows for blocks to be produced without relying on mining hardware. As such, instead of competing for the next block with heavy computation work, PoS validators are selected based on the number of coins they are committing to stake.Users that stake larger amounts of coins have a higher chance of being chosen as the next block validator. Staking ExplainedStaking requires a direct investment in the cryptocurrency, while each PoS blockchain has its particular staking currency.The production of blocks via staking enables a higher degree of scalability. Moreover, some chains have also moved to adopt the Delegated Proof of Staking (DPoS) model. DPoS allows users to simply signal their support through other participants of the network. In other words, a trusted participant works on behalf of users during decision-making events.The delegated validators or nodes are the ones that handle the major operations and overall governance of a blockchain network. These participate in the processes of reaching consensus and defining key governance parameters. Read this Term using its own financial infrastructures, such as MetaMask Institutional and Codefi Staking.

MyCrypto Acquisition

Recently, ConsenSys announced the acquisition of MyCrypto, a market-leading Web3 wallet. Following the acquisition, ConsenSys will combine MyCrypto with its popular MetaMask wallet.

MetaMask and MyCrypto will integrate their efforts under a shared brand to enhance the security of all their products and build a cohesive user experience across browser, extension, mobile and desktop wallets.

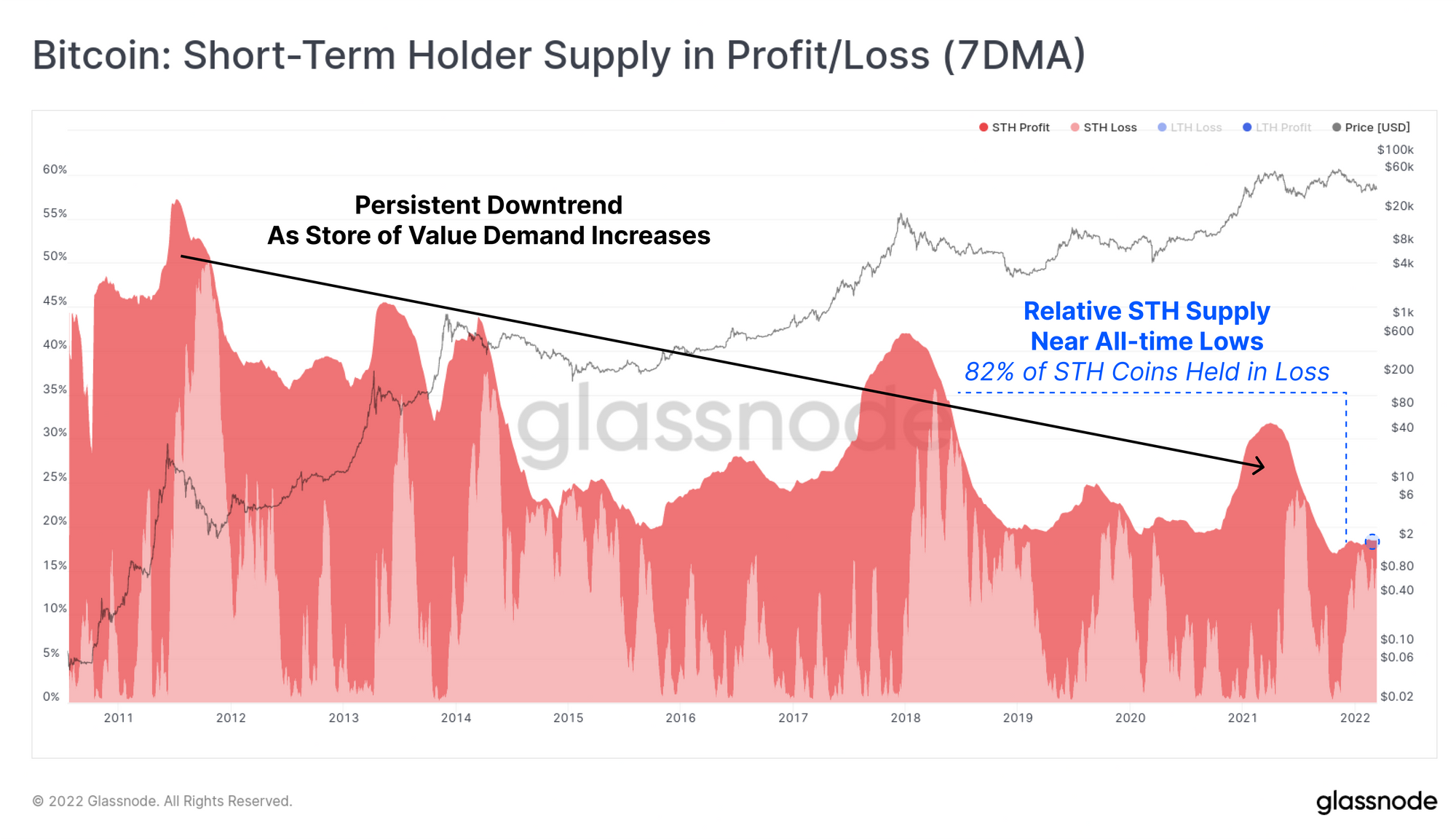

On-chain data shows around 82% of the Bitcoin short-term holder supply is currently in loss, suggesting that capitulation may occur soon.

82% Of Bitcoin Short-Term Holder Supply Now In Loss, While Total STH Supply Declines

According to the latest weekly report from Glassnode, the BTC STH supply is nearing all-time lows at the moment. However, 82% of it is being held at a loss.

The “BTC short-term holder supply” is that part of the total Bitcoin supply that has been held for less than 155 days.

The investors holding this supply are usually the likeliest to sell their coins off during market volatility, and especially when a capitulation flush out occurs.

An on-chain indicator, the Bitcoin STH supply in profit/loss, tells us the percentage distribution between these coins being held at a profit and those being held at a loss.

When a high amount of this supply is in loss, there may be more sell-side pressure in the market as short-term holders capitulate easily.

Related Reading | Bitcoin MPI Rises To Highest Value Since March 2021, Bull Rally Soon?

Now, here is a chart that shows the trend in the BTC STH supply over the history of the coin:

Looks like the value of the indicator has declined over the years | Source: Glassnode's The Week Onchain - Week 11, 2022

As you can see in the above graph, the Bitcoin STH supply has been observing a constant downtrend over much of the history of the coin, and is currently near all-time low values. The decrease in this supply happens when some of the coins mature beyond the 155-day cutoff, thus becoming part of the “long-term holder supply” instead.

Since short-term holders can be a big source of sell-side pressure, the number of coins held by them severely going down can be bullish for the price of the crypto.

Related Reading | Bitcoin Hashrate Swells 15% Since Last Week As Analysts Expect Mining Difficulty To Increase

However, while the supply is low right now, around 82% of it is currently in loss. So despite the decline in total supply, these coins in loss still amount to around 2.5 million BTC, and thus they can add quite significant sell pressure to the market.

As macro uncertainties like the Russian invasion of Ukraine continue to loom over the Bitcoin market, these short-term holders may finally break and capitulate in case their coins remain in the red or go even deeper.

BTC Price

At the time of writing, Bitcoin’s price floats around $38.5k, down 1% in the last seven days. Over the past month, the crypto has lost 10% in value.

The below chart shows the trend in the price of BTC over the last five days.

BTC's price seems to have been in consolidation for a few days now | Source: BTCUSD on TradingView

Featured image from Unsplash.com, charts from TradingView.com, Glassnode.com

Over the past week, long-term holders of Bitcoin increased their spending to a level that suggests de-risking from the market, but hodling remains the predominant investing strategy.

Uncertain macroeconomic headwinds are likely to have precipitated the increase in the sell-offs last week by long-term holders and shaken some short-term holders out of their positions according to data from blockchain analytics firm Glassnode. Last week, coins older than six months accounted for 5% of total spending, which is a level not seen since last November.

Short-term holders (STH) who have held coins for less than 155 days continue to decline in number, but not necessarily due to selling. Glassnode suggests that while it is generally more common for STH to sell, the recent decline in STH supply “can only occur when large portions of the coin supply are dormant and crossing the 155-day age threshold, becoming Long-Term Holder supply.”

Bitcoin (BTC) accumulation patterns do not suggest bear market behaviors yet as overall sell pressure remains consistent. Also, more than 75% of the BTC circulating supply has been dormant for at least six months despite the recent uptick in selling. Glassnode says this is an indication that investors are still predominantly hodlers.

Long-term Bitcoin holders increased selling last week. – Glassnode

Glassnode noted that the sell-offs have been into a relatively strong market that has avoided any significant moves up or down and has remained range-bound for most of this yea. This is thought to be staving off a capitulation event which often comes at the end of a bear cycle. There has not been a significant capitulation since last May when BTC price crashed from $58,771 to $34,977 over the course of a 15-day period according to CoinGecko.

The period from the May capitulation event until October marked the last time BTC accumulation resembled bear market behavior.

BTC accumulation patterns are still above bear market trends. – Glassnode

The profit/loss ratio of STH supply is still near the all-time low set in mid-2021. Currently, 82% of STH coins are being held at a loss which Glassnode states is an indication of the later stage of a bear market when savvy investors send their coins to cold storage to lie in wait for the return to positive profit margins.

Short-term holders are in near-record losses. – Glassnode

Related: BTC price struggles below $39K ahead of expected interest rate hike by the Fed

As noted in last week’s BTC market update, exchange outflows remain quite high. Coinbase saw its largest outflows in nearly five years last week with 31,130 BTC leaving the exchange. These outflows illustrate Bitcoin’s increasing reputation as a must-have in a modern investor’s portfolio, and a further reluctance to liquidate in a hurry.