[ad_1]

Not your typical Bit Media Buzz but we thought we’d share 😊

Continue reading on Medium »

[ad_2]

Source link

[ad_1]

Not your typical Bit Media Buzz but we thought we’d share 😊

Continue reading on Medium »

[ad_2]

Source link

[ad_1]

It’s unquestionable that the future of mankind is one filled with machines, IoT devices, and robots. Be it sensors, drones, assistant robots, they’ll all be generating abundant amounts of data through their activities and interactions with humans. Much of their generated data will be valuable to both individuals and companies.

Just take a few moments to imagine a future for yourself where you’d be able to monetize valuable data created by your robotic devices and turn that into a source of income by tokenizing it on the blockchain. Or one where your automated home environment can autonomously purchase or process helpful data to do its job better and make your life more convenient.

A collaboration between Robonomics, a platform for developers and engineers to connect IoT and ROS compatible devices to a digital economy and Ocean Protocol, which lets one monetize any kind of data is creating a future where machine data can be automatically monetized.

Through the use of Robonomics, IoT devices and robots can become economic agents for people. Simply put, they can partake in legal obligations, purchase things, and even participate in an open job market.

As mentioned previously, a robot economy naturally produces a lot of data, this is where Ocean comes in. Robonomics leverages Ocean Protocol and the creation of data tokens, a fundamentally new type of asset, to discover new pathways and use cases for automatically monetizing data generated by robots and IoT devices.

With a growing robotics and automation trend in everyday life, it is now already possible to quite easily see potential applications of such technology. An important and demanded one is the tokenization of environmental data obtained from a device, for example, a sensor or drone that measures soil, air, and water pollution.

The ability to tokenize and monetize such environmental data will allow for the emergence of new markets that revolve around concepts of carbon credits and citizen science. If we take into account a growing interest in pollution, environmental friendliness and management, then quite a bit of value can be attributed to this data. And the value of it will only continue to grow.

We all interact with autonomous systems quite frequently in our daily lives while often paying no attention to it. For instance, we’ve all likely been in contact with a robotic customer service agent on the phone or online. There is valuable data in such interactions that could be tokenized for marketing and consumer relations purposes.

As the trend of IoT and robotics involvement in our daily lives continues to grow, so will use cases for the tokenization of such data. Imagine robot waiters or public service workers and the audio, visual, and any other data they collect when executing any given task like serving or helping a customer. If such a robotic waiter or worker was live on the Robonomics network, its data could be collected and further analyzed with machine learning and various algorithms, tokenized, and sold to those who need it.

The use cases presented are no more than but a little food for thought of what can be achieved through the Robonomics Network and Ocean Protocol collaboration. As IoT and robots continue to proliferate, entirely new avenues for the use of their data will emerge. And both projects are essentially ushering in a new market for cyber-physical data and will be at the forefront of it.

[ad_2]

Source link

[ad_1]

AscendEX, a cryptocurrency exchange platform, announced it has partnered with BANXA to offer a zero-fee rate for users to buy crypto with their credit card/debit card. This promo is concurrent with other fee-free bank transfer payment methods. Active since July 6th, the zero-fee event will last for 14 days.

July 6th, 12 a.m. UTC through July 21st, 12 a.m. UTC.

[ad_2]

Source link

[ad_1]

Crypto-focussed Swiss bank, Sygnum Bank, has announced it has become the first bank in the world to allow its clients to stake Ether.

According to the July 6 blog post, the firm’s clients can now stake ETH through Sygnum’s institutional banking platform to earn yields of up to seven percent annually.

Sygnum describes itself as the “world’s first digital asset bank,” having secured a banking licence in Switzerland and a capital markets services license in Singapore during August 2019 and October 2019 respectively.

The firm asserts that “the vast majority of decentralized products and services run on Ethereum,” noting the DeFi sector’s Total Value Locked (TVL) has grown by more than three times since the start of 2021:

“With Ethereum powering the exponential growth of decentralized finance (DeFi) applications, staking is a compelling choice for long-term Ethereum investors also seeking attractive yields.”

Thomas Eichenberger, Sygnum’s head of business units, described Ethereum staking as “a core element for digital asset portfolios.”

Sygnum launched a staking service for Tezos (XTZ) in November 2020, and has offered a fixed term deposit product for its Digital Swiss Franc stablecoin, DCHF, since March.

The bank faces competition from many crypto-native staking providers and centralized exchanges, including leading U.S. firms Coinbase and Kraken.

The digital asset bank is also looking to support DeFi assets, launching regulated banking services for eight leading tokens including UNI, MKR, and CRV last month.

According to Staking Rewards, Eth2 is currently the second-largest Proof-of-Stake network by staked capitalization with $13.5 billion, despite only 5% of circulating Ether currently having been locked for staking.

Cardano (ADA) has the largest staked capitalization with $31.8 billion and 70.7% of supply currently locked.

[ad_2]

Source link

[ad_1]

In the recent live streamed AMA hosted by next generation mobile crypto cold wallet ELLIPAL, increasingly popular smart yield optimizer…

Continue reading on Medium »

[ad_2]

Source link

[ad_1]

For many people, financial technology is somewhat incidental. It is a passing part of daily life: we interact with fintech when we send money online, check our bank balances with our mobile phones, or use an app to buy cryptocurrency.

However, for much of the world fintech is so much more. Financial technology can and will play an important role in the ways that societies develop. With the advent of internet accessibility, fintech is reaching a larger group of people than ever before.

Bank Account Alternative. Business Account IBAN.

Here are some of the most important ways that fintech itself is changing, and that fintech is changing the world.

In the earlier days of financial technology, systems architecture was often created in a monolithic fashion: systems were built as a single unit, only alterable by making changes to the source code. In some cases, this kind of design meant that if part of a financial services system went down, the entire thing could be compromised.

Microservice architecture was designed to make digital financial services more flexible and secure. This kind of system design breaks down monolithic structures into smaller, independent services that can be deployed for specific purposes.

For example, an older system design could consist of a payments service, a credit auditing service, and an international money transfer mechanism that were all combined into a single piece of software. If the company that operated the software wanted to change the credit auditing service, it would have to update the entire system at once.

However, with a microservice architecture, the payments service, a credit auditing service, and an international money transfer mechanism could still operate within the same ecosystem as separate, independent entities. Therefore, if the system operator wanted to make changes to the credit auditing service, it could do so without disturbing any of the other pieces of the system.

While this architectural concept can be applied in the world of centralized financial services, it seems to borrow from the concept of ‘money legos’ that came from the decentralized finance (DeFi) sphere.

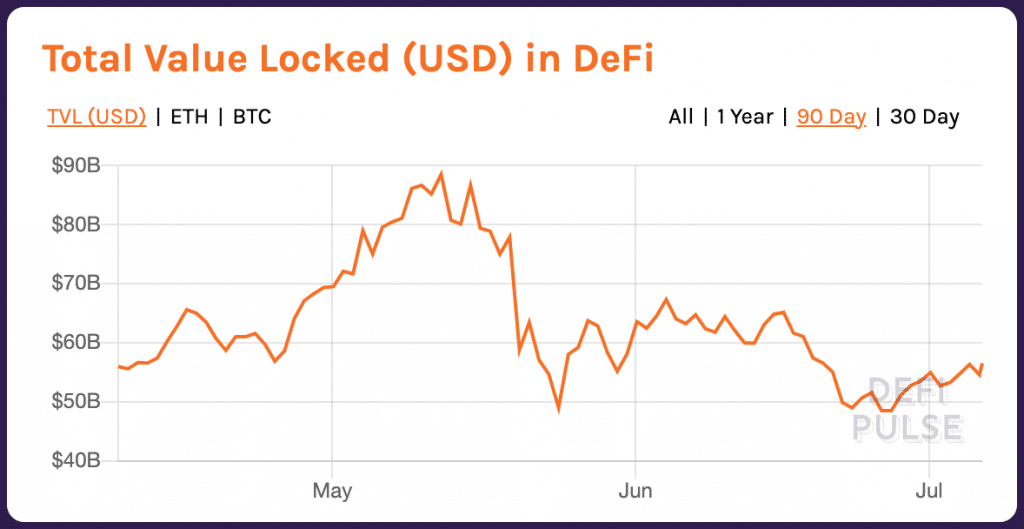

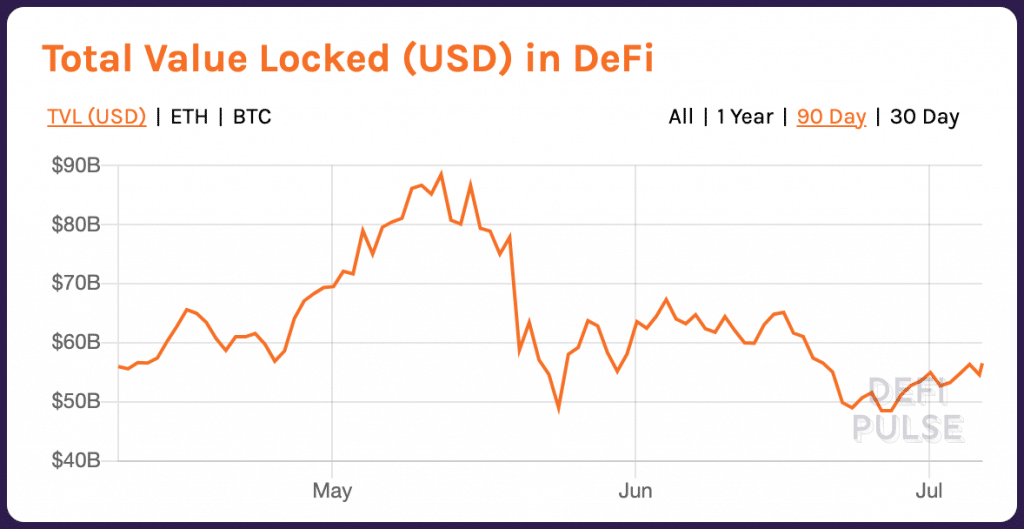

Seven months into 2021, decentralized finance is bigger than it has ever been. At the beginning of the year, the total value locked (TVL) in the DeFi ecosystem was equivalent to roughly $20 billion; today, DeFi’s TVL is roughly $56 billion. At its peak in May, the TVL was roughly $90 billion.

As the size of the DeFi ecosystem continues to grow, so too have the number of DeFi use cases. DeFi platforms have been built for asset management, digital identity, insurance, derivatives, synthetics assets, digital asset exchanges, analytics, risk management tools and more.

Because of the risks associated with many decentralized finance platforms, institutional players have largely stayed out of the DeFi world. Therefore, the vast majority of DeFi’s growth has come from retail users and investors.

However, some platforms are taking steps to create the infrastructure to support the entrance of institutional players into DeFi. For example, DeFi lending platform Aave announced earlier this week that it will be launching Aave Pro, a permissioned platform that will support institutional usage. Aave said that the launch is coming in response to ‘extensive demand from various institutions’.

Artificial intelligence and machine learning have a variety of use cases across financial technology. However, one of the most prominent use cases is monitoring, analyzing and predicting customer behavior. For example, AI can be used to determine how and when users of an online banking service might run into technical trouble, and then offer assistance through a chatbot.

Swiss Fintech Set to Change the Landscape of Isolated Financial ServicesGo to article >>

The use of AI and machine learning is expected to continue to grow with regard to financial regulations and policy compliance, algorithmic trading and fraud detection. AI systems can also play an important role in financial institutions’ anti-money laundering and counter-terrorism operations.

According to Planet Compliance, “the sectors that are expected to be most affected include insurance, financial data, asset management, decentralized exchanges and lending.”

The climate crisis has wreaked havoc in much of the world, and many new areas that were previously unaffected by climate change have recently undergone serious incidents. For example, the Pacific Northwest is currently in the midst of the worst heat waves in recorded history.

As a result, everyone is expected to do their part in the battle against climate catastrophe. This has touched the financial world in a fairly significant way: for example, some cryptocurrencies have been under fire this year for their heavy energy consumption.

Therefore, it is likely that financial technology companies across the board will be increasingly expected to demonstrate their sustainability initiatives.

Fintech companies and financial institutions may be held to a higher standard in terms of who they do business with. Dr Thomas Puschmann, Director Swiss FinTech Innovation Lab, said in a recent interview with Finance.Swiss that for example, in the lending sector, “[banks] need to know what firms are investing in sustainable solutions for the future.”

However, there are some significant challenges in terms of sustainability data collection that could guide the decision-making process of many fintech firms and banks.

“Take, for example, the value chain of a company. Today, we know the greenhouse gas emissions that a firm emits, these so-called Scope 1 emissions and Scope 2 emissions. Scope 1 are the ones that come out of your house; Scope 2 are the ones that you purchase in the form of energy from your energy provider; but Scope 3 emissions, which very often make up to 75 percent of all greenhouse gas emissions, come from anywhere in the supply chain that you can’t control and don’t even know it.”

“So you need data for that to decide if you want to lend money to such a firm,” he said.

Cryptocurrency and decentralized finance have long been slated as technologies that can provide financial services and opportunities to users in developing markets. However, the opportunity to take root in emerging economies is open to fintech companies.

In 2021, there has been massive unmet demand for financial services in the developing world. At the same time, the number of smartphone holders in emerging markets is continuing to increase This presents an important opportunity for fintech companies that can provide mobile-based services to users in untapped markets.

In an article entitled “Fintech and Sustainable Development: Assessing the Implications,” authors Juan Carlos, Castilla-Rubio, Nick Robins and Simon Zadek said that financial technology can support the growth of developing markets by “[unlocking] greater financial inclusion by reducing the costs for payments and providing better access to capital domestically and internationally.”

Moreover, the paper said that fintech can “Provide financial markets with the level playing field and market integrity needed for long-term real economy investments aligned with the sustainable development agenda,” among other things.

These are just a few of the ways that developments in financial technology are changing financial services as we know them.

What are your thoughts on the ways that fintech is impacting the world around you? Let us know in the comments below.

[ad_2]

Source link

[ad_1]

An ex-employee of the now-defunct crypto exchange Cryptopia has admitted in court to stealing crypto worth about $170,000. The employee pled guilty to stealing coins and customer data while he worked at Cryptopia when the company was still up and running.

A name suppression by the Christchurch district court of New Zealand keeps the employee anonymous for the time being. The employee pled guilty to two crimes, namely; theft by a person in a special relationship and theft of more than $1,000.

Related Reading | Robinhood Fined $70M For Causing “Significant Harm” To Customers

The crime was brought to light in 2020 due to complaints from a customer that he had deposited coins into a Cryptopia wallet by mistake. Cryptopia has been through a series of problems in the past. Which is what led to its now-defunct state. The company finally collapsed in 2019.

Cryptopia suffered two devastating hacks that eventually led to it shutting down in 2019. The company was hacked at the beginning of 2021 in January when a hack led to the theft of over 19,000 Ethereum. The crypto was transferred into an unknown wallet. The value of the crypto at the time of the hack in 2019 was $2.3 million. At this point, Cryptopia was serving a global customer base of 1.8 million customers.

Crypto subsequently went into liquidation that year and began the process of shutting down the exchange and mapping out ways for users to get their crypto back.

Bitcoin price loses momentum as it falls back into $33K range | Source: BTCUSD on TradingView.com

Later that year though, the company fell victim to another hack. This time losing about $15 million worth of crypto to the attackers. The hack happened during the liquidation. Somehow attackers were able to access a wallet that had not fallen victim to the hack and transfer the crypto out of that wallet to an unknown wallet. This hack represented about 15% of the company’s holdings of digital assets.

During the liquidation, employees of the company were terminated. But not before an employee had copied private keys and customer data. These he retained after his employment with the company were terminated.

The data available to this single employee reportedly gave him access to over $100 million worth of digital assets.

Having access to the keys, the employee believed that no one would check old transactions during the liquidation. The employee had transferred Bitcoins with the equivalent value of approximately $160,000 out of wallets and over $100,000 worth of other cryptos.

While he was employed at Cryptopia, the employee had made copies of Cryptopia’s private keys and customer data. He stored this on a USB flash drive. Which he then took home and uploaded the data onto his personal computer at home.

Upon finding out that old transactions were in fact going to be reviewed, the employee came forward to admit the theft. According to the employee, he had planned to return the crypto over time. And he had apparently taken the crypto because he was frustrated with the company, Cryptopia.

Related Reading | Bitcoin Whale Warns Of “November 2018 Vibes.” What This Means

The employee also admitted that he had believed he would get away with the theft as he did not think that anyone would go on to check old transactions.

Upon stepping forward, the employee had sought assurance that he would not be persecuted for the offenses. Although he has now been arrested and charged and will remain in jail until his sentencing, which is scheduled for October 20th, 2021.

The crime is unrelated to the Cryptopia hack. The employee has returned some of the cryptos and has promised to pay back the rest over time.

Featured image from PCMag, chart from TradingView.com

[ad_2]

Source link

[ad_1]

Decentralized lending protocol Aave is planning to launch “Aave Pro,” a permissioned platform for institutional investors later this month, according to a new report from Cointelegraph. The platform, which will provide the same kinds of services as Aave’s current platform, will be launched in partnership with the digital asset custody and settlement platform Fireblocks.

The new platform was reportedly announced in a webinar entitled ‘Next Steps in Institutional DeFi’ that featured Stani Kulechov, Michael Shaulov and Mike Novogratz, who are respectively the CEOs of Aave, Fireblocks and Galaxy Digital.

Bank Account Alternative. Business Account IBAN.

According to a screenshot of an email that is said to recap the contents of the webinar, Aave is launching Aave Pro in response to ‘extensive demand from various institutions’. The platform will only support four crypto assets in the beginning: BTC, ETH, AAVE and USDC. Additionally, Aave Pro’s pools will be kept separate from its main platform. Further, the email said that there are plans to eventually decentralized the governance of Aave Pro.

$AAVE Pro coming in July.

For those that didn’t attend the “NExt Steps in Institutional Defi” Zoom with Stani, here’s a recap email I received. pic.twitter.com/ClwlBkXh2r

Suggested articles

How Customer Retention Can Transform Profitability & Brand PerceptionGo to article >>

— Noah (@TraderNoah) July 4, 2021

In addition, Aave Pro will add a whitelisting layer onto Aave’s V2 smart contracts to ensure that only ‘institutions, corporates, and fintechs’ approved by Fireblocks’ Know-Your-Customer verification process can access the platform. Moreover, Fireblocks is responsible for Aave Pro’s anti-money laundering and anti-fraud controls.

Aave Pro is slated to vastly expand the total value locked in the Aave ecosystem, which currently sits at around $17 billion.

According to CoinTelegraph, the announcement of the new platform received ‘mixed reactions’ on Twitter. Some enthusiastic users pointed out that the platform will act as a rail for institutions entering the DeFi world in a meaningful way for the first time.

However, others pointed to an ongoing lawsuit against Fireblocks by staking provider StakeHound. The lawsuit was filed over the alleged deletion of private keys to a wallet that contained $72 million in ETH.

Aave first announced that it was entering the institutional world in May, when Kulechov said that Aave had created a “private pool” for institutions to “practice” with before jumping headfirst into DeFi. Furthermore, Aave partnered with Compound in early 2020 to launch DeFi services for institutional investors.

[ad_2]

Source link

[ad_1]

The Philippine Stock Exchange (PSE) is aiming to be first in line when financial regulators give the green light for crypto asset trading in the country.

On Friday, July 2, CNN reported that PSE president and CEO Ramon Monzon said the local bourse should be the country’s first exchange platform for crypto assets. He stated:

“If there should be any exchange for cryptos, it should be done at the PSE. Why? Number one, it’s because we have the trading infrastructure. But more importantly, we’ll be able to have investor protection safeguards especially with a product like crypto.”

The country’s stock exchange is now awaiting guidelines from the Philippine Securities and Exchange Commission and other financial regulators.

Despite his eagerness to support crypto asset markets, Monzon warned of crypto’s volatility, stating: “instant riches could be instant poverty too.”

Related: Crypto in the Philippines: Necessity is the mother of adoption

Government regulators in the Phillipines began researching regulating crypto asset trading in 2019 when the SEC sought feedback from banks, investors, and the public on whether the country was ready to build a fully-fledged cryptocurrency exchange.

Local demand for digital payments is strong, with as much as 10% of the GDP coming from remittances from an estimated 10 million expatriate Filipinos working overseas.

The Philippines has sought to establish itself as a regional hub for crypto in recent years, opening its Special Economic Zones in Cagayan to crypto firms in 2018.

In January, the central bank established new guidelines for crypto asset service providers after witnessing accelerated growth in the use of digital assets over the past three years.

[ad_2]

Source link

[ad_1]

Polygon has announced the integration of yield optimization vaults on the Maker Network. The blockchain-enabled protocol, formerly referred to as the Matic Chain, tweeted on Wednesday that it “will be opening a vault on Maker” and investing $50M of MATIC tokens as agreed liquidity from the treasury.

With the recent integration, it means the protocol has now broadened in scope, vision, and transformation to become an Ethereum scaling aggregator.

Related Reading | Scaramucci’s Skybridge Capital Launches Ethereum Fund

Such feet, among others, would see the protocol network providing developers with L2 solutions. This will be in addition to the POS/Plasma chain – mainnet, launched in April 2020.

Polygon provides the core components and tools to join the new, borderless economy and society. Two key platforms materialize it: The polygon framework and the Polygon protocol.

With these technologies, any project can quickly spin up a dedicated blockchain network that combines the best features of “stand-alone blockchains (sovereignty, scalability, and flexibility) and Ethereum (security, interoperability and developer experience).”

Plus, these blockchains are friendly with all the existing Ethereum tools such as Metamask, MyCrypto, Remix, etc. So again, the exchange of information among themselves and with Ethereum is facilitated.

Related Reading | Why Terra (LUNA) Will Reward Users With New Community Bounty Program

Summary: Polygon is a blockchain protocol and a framework for creating and connecting Ethereum-compatible blockchain networks.

One is collapsing together scalable solutions on Ethereum and supporting multiple chains in the Ethereum ecosystem.

MATIC, the native token of Polygon, is an ERC-20 token running on the Ethereum blockchain. The tokens are used for payment services on Polygon and as a settlement currency between users who operate within the Polygon ecosystem.

MATIC set to follow an upward trend in the daily chart. Source: MATICUSD Tradingview

This has turned out to be quite positive for the MATIC community as the token as hovering in the green-zone marking 1% of growth at the time of writing this article.

As an integral part of the announcement, $50M of MATIC tokens have been committed by Polygon on the newly opened vault on Maker.

MakerDAO is an organization developing technology for borrowing, savings, and a stable cryptocurrency on the Ethereum blockchain.

It has created a protocol permitting anyone with ETH and a MetaMask wallet to loan themselves money in the form of a stable coin referred to as “DAI.”

Related Reading | Ethereum Upgrades Could Jumpstart $40 Billion Staking Industry, JP Morgan

By integrating loans with a stable currency, MakerDAO typically allows anyone to borrow money and reliably predict how much they had to pay back. This alleviates the fear that used to come in the era of crypto to crypto borrowing.

Polygon board, opening a vault on Maker and committing $50M of MATIC tokens as seed liquidity from the treasury, sincerely thanks the MakerDAO community and team.

They appreciate the effort to quickly process the entire governance activities/polls and their feedback to onboard MATIC as collateral.

“This is a crucial development in Polygon’s long-term vision and commitment to develop the Ethereum scaling landscape and entice the gifted builders and engaged community members,” the board reveals.

Following this, Polygon will be minting DAI, which will invest in the Ethereum ecosystem.

Similarly, there are few other networks opening vaults on polygon technology. Beefy Finance, for instance, launched its first Beefy yield optimizing vault In Polygon on the 28th of April, 2021.

The finance tech is a Decentralized, Multi-Chain Yield Optimizer platform that allows its users to earn compound interest on their crypto holdings. In addition, it has launched a new Ape Swap vault deployed on Polygon.

Despite the attractiveness, there have been some skeptical postures on the project.

Many keen crypto lovers and observers are quarrying that, If approved, would Polygon utilize this class of vault themselves?

Are there any specifically identified users – individual or entity – who have expressed an intention to use this class of vault if MakerDAO onboarded this collateral? Well, for now the MATIC community seems to be appreciating the latest development.

Featured image from Pixabay, chart from TradingView.com

[ad_2]

Source link